WHAT DO THEY KNOW OF ENGLAND?

Let us look at tech, private equity and this seeming market bounce, driven by those sectors. The NASDAQ is up almost 10% at 11,320 after a trio of twelve-month lows in the mid 10,300’s, the latest of those lows just this week. Meanwhile it looks like the US Elections have delivered both gridlock and a rebuff for Trump, which some see as a perfect mix.

Today’s post title is derived from Rudyard Kipling at his most sanguine and reflective.

I HAVE FLUNG YOUR STOUTEST STEAMERS TO ROOST

The true horror of the tech wreck has also been concealed for UK investors, by the climb in the dollar, a move that seems to be going into reverse. In terms of closing prices sterling has rallied hard from 1.08 to 1.18 in a little over a month. This has left the NASDAQ collapse, from touching 16,000 - brutally exposed, now without much of the concealing currency appreciation.

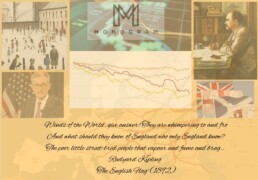

Where is the Nasdaq headed?

We suspect that the NASDAQ is heading lower still, but accept that is a big call.

From this page on Tradingeconomics

It remains a crowded space for a lot of unprofitable companies to jostle, as they build market share. This disguises the possibility that in some spaces, even owning the entire market will still be loss making.

However, market sentiment has perhaps turned, the tech rubbish generally got chucked out early. The subsequent switching out of the tech majors probably had to be into Treasuries, where their recent price rises suggest some demand, or into cash.

It remains a crowded space for a lot of unprofitable companies to jostle, as they build market share. This disguises the possibility that in some spaces, even owning the entire market will still be loss making. Bumping up against that is the second phase of the market collapse, as the multiples on profitable tech giants returned to earth.

And cash (and oddly apparently the S&P) has also been seeing inflows from China and crypto, as those areas have sold down hard. There is also the unpleasant negative impact of holding cash, on returns. Put this together with sentiment, and this may well help the NASDAQ bounce into the year end. However, many fund managers cite the dotcom bust as meaning this is now starting a multi-year sideways recovery phase, not a quick bounce at all.

LONG BACKED BREAKERS CROON

A concurrent look at Private Equity is important. NASDAQ multiples drive much of their values and are falling, and with such a recent twelve-month low, Q3 valuations (private equity valuations are always lagged) have further losses built in. And a sprinkling of those will now also be based on a significantly higher dollar too. That won’t be pretty either.

Plus, as we know there are some spectacular blow ups lurking in there, the insolvent FTX was a big investor in, and investee company for, some well-known PE names. Overall, despite solid reports, I am still expecting some fair-sized holes in quoted private equity, as either the NASDAQ rises and the dollar falls, causing currency losses, or the NASDAQ falls and the dollar rises and the one again masks the other.

Access to distress financing, has it seems largely vanished, as it does at times like this, making the chance of highly damaging wipe outs, not just down rounds, much greater.

A possible dollar sterling parity?

But those talking of dollar sterling parity are surely way off now. So, regardless of future disasters, I want more information before seeing UK Quoted Private Equity Investment Trusts as a buy. About six months after the NASDAQ bottom, will be a good valuation point, and that likely means Q3 2023. At that point we will know what the current large discounts really refer to; I don’t expect them to look anything like as generous.

THE UK - UNDER A SHRIEKING SKY

There is a lot of market optimism about the next UK budget, based on Hunt being really nasty. That may overstate his hand, as the Government has long abandoned reform, it can only support out of control spending by harsh tax rises, which will certainly kill jobs, but probably the wrong ones.

Nor can it do much to enhance investment and has foresworn labour market reforms, so both of those, with existing policies and more rate rises, must encourage the persistence of poor productivity.

Although of course the real budget numbers will be barely mentioned; energy, rate rises, and inflation are largely out of Hunt’s hands. He is lucky all three do look a lot better than when he was installed. So, the need for harsh medicine is rather reduced, and may even disappoint.

But just as the rally helped US risk assets, so it helped others, like property, come off a deeply oversold floor. TR Property Investment Trust has jumped 30% in a month, for example, and still yields over 4%.

Post Mid-term elections for the US

And coming full circle, although slowing inflation took a lot of the credit, at least some of the post Mid Term bounce came from realising that the Federal Reserve now has an ally in the legislature. It can be less vigorous in steering the economy, just relying on the brake pedal, as Biden and Congress are no longer able to simultaneously hammer the accelerator.

Overall, however we still remain cautious, we expect this pre-Christmas rally to fade, rate rises to persist into at least Q2 2023 and rate cuts to be a 2024 feature. And peak gloom lies ahead as those rate rises conclude and then start to actually bite.

Looking ahead

In general markets have had a solid look at the worst case this year, from famine to invasion and nuclear war, to out-of-control Central Banks and deluded politicians, and nothing terribly dramatic has transpired. So even with bad things still happening, we don’t see a repeat of this year’s dramatic falls either.

Charles Gillams

- The Kipling Society meets on November 16th, at the Royal Overseas League.