WE ARE NOT NOW THAT STRENGTH

Markets are confused, as are Central Banks, and while generally indifferent to small wars, we know that’s how large wars start. And we have another month till November 5th and the US election. In the UK the Chancellor says it is all terrible, but is splashing cash around with abandon, but then cancelling dozens of projects, and claiming she is pro-growth, while taxing investment ever harder and encouraging so much capital flight even the OBR has noticed.

The colossal COVID debt burden still hovers over everything, a burden that can only be shed by growth or inflation, one an investor’s friend, the other their mortal foe.

Market confusion is more about politics than economics, no US rate cut in July, then a double cut in September, now a November (post-election) cut looks uncertain. The stated reason for a double cut was weak employment, but the real reason was political. Powell even said in his press conference that the Governors voted for the jumbo cut “in the best interests of the American people” so not economics, and I suspect those archetypal insiders will believe keeping Trump out is exactly that.

So, we get a “value” rally, as collapsing labour markets would lead to multiple rate cuts, and market interest rates, surprised at the severity, then overshoot on the downside.

Except there is little evidence of anything wrong in US labour markets, as Friday showed, they are fine, and wages, along with rigid labour markets are driving inflation. Weird. But then good labour markets, plus buoyant earnings, plus falling rates sounds pretty good for equities?

Plus, something most odd in China, which from nowhere became one of the top markets in the last year, outperforming the major UK averages. Yet no one is clear why, on fundamentals. Yes, there was a stimulus package, possibly one focused on equities, possibly bigger than expected, but no one thinks it solves anything.

So, it (and ripples into luxury and metals) seems an almighty short squeeze. China had become so unloved, even its proudest fans had bailed out. The rush back in left other emerging markets, like India, struggling.

[Culled from two pages on Yahoo finance – read more here and here]

MANNERS, CLIMATES, COUNCILS, GOVERNMENTS.

Meanwhile, the Tory Conference was oddly upbeat, with some real choices, and a fair bit of optimism. The Tory party is in theoretical retreat, but greatly energised by a real debate, with members involved, about the new leader and a new direction. The disastrous election result had focused minds nicely, and yet was still discounted. Starmer had won fewer votes than Corbyn, and his popularity was already below Sunak’s. The loss was about “three tens”; voters switching to Reform, to the Lib Dems and the Sofa, sitting it out.

None of that was the love of another party, all of it was hatred of those Tories, divided and incompetent and now gone. In so far as the rump of the party now had stars, they were all standing for leader, no big guns were left after the disaster.

It was generally agreed that it must be the fault of Central Office and candidate selection, not the Party. The conference was also largely devoid of the usual big brother manipulation, fake applause, dire autocue speeches approved by a SPAD and ministers just too busy to care.

Tugendhat was bouncy, had the youth vote and the best video, but not convincing. Cleverly had worked hard, was fun and avuncular, relaxing and the obvious unity candidate. Jenrick gave some very strong speeches, plenty of thought, but seemed off-form and weary at the closing main event. Badenoch is an enigma, slightly thrown by adding “2030” to her pitch, when everyone was suddenly thinking “2029” again. Yet she is the one who wants to reform, draw a line below the stale “what did we do last time” and start afresh. She had the best merch too.

It is still a split party, for all that. A good chunk of the younger party is very keen on Net Zero, and they were extremely visible, indeed Net Zero before all else. However the MPs know that was a Cameron fantasy, so I am not sure how that plays out.

But also, a clear understanding that talking right, governing left is finally over, and that border security is high priority, and defence is too, but not with quite the gung-ho optimism of before.

In many ways Starmer’s inability to know what sleaze and greed looks like, even if it is all innocent (a big even) bodes ill for his time; “they are all the same” is a deep-seated rallying cry of pain.

THE SCEPTRE AND THE ISLE

I am enjoying “The Sale of the Late King’s Goods”, a slightly wonkish account of Charles I’s lost trophies, but an excellent canter through the lead up to the English Civil War. It is striking how state policy was all so plausible and desirable, except for a massive inconsistency on faith, finance and Europe.

The King was desperate to be trendy, to think common decency only applied to others, had no real conviction, in restlessly appeasing various European Courts, seeking favours that never came. While funding was all about just getting to the next OBR review with enough cash to pay off friends. (Well OK, not the OBR back then, but a truly sovereign Parliament).

After finding so many conflicting aims inevitably failed to work, he then tried to drag Scotland into a standard set of beliefs and rules, and hoped blindly that the Irish would do us a favour. The desire to be liked, to look good, to look to Europe for answers, to throw money at white elephants and foreign wars, and the absurd doctrinal battles, all felt far too familiar.

If we don’t know where we are going, just buying expensive tickets won’t complete our journey. To strive, to seek.

The title of this piece comes from Ulysses, a poem by Alfred, Lord Tennyson

https://poets.org/poem/ulysses

Andrew Hunt’s piece this month, which looks at the solidity of underlying data and China may be of interest to serious investors.

Tiptoeing Through the Tulips

Is real estate safe yet? How about renewables? And an innocuous Tulip.

All three of this week’s topics are notable for what they are not, Real Estate valuations do not reflect property markets or indeed replacement cost, Renewable Energy valuations do not reflect anything much, but include plenty of hope, and the new City Minister seems to have no obvious purpose beyond being a safe and reasonably loyal supporter of all things welfare related.

Unreal Estate

As we have remarked before, somehow the RICS valuations of property assets, used to value quoted property companies, became heavily reliant on interest rates and comparable bond yields and rather less interested in the real property market. They also seem to have become a tool for bank lending, disregarding other more real-world factors. Which explains the paradox of falling valuations alongside robust occupancy levels and a level of visible new office construction, certainly in London, which remains unabated and indeed the wider market is seemingly indifferent to the slump.

There is a lot behind those paradoxes, long lead times through planning, the desire to replace older stock if (as so often) it is to be leased out, the dominance of bank funding, not equity. Even so both collapsing valuations and the discounts then applied, have been damaging. This has been exacerbated by underlying fears about vanishing bank financing, in many ways a self-fulfilling prophecy.

We had something of a buyer’s strike where vendors can’t get bank finance to stay, and their potential buyers can’t finance to buy. The impact of working from home and the inevitable changes in business models adds to this.

Some areas, notably much of Docklands and many regional and secondary offices, have become untouchable. Closed end property vehicles have been forced to sell to meet bank covenants, and several open-ended ones have simply been forced to liquidate. Something of a perfect storm.

Yet, prime real estate has in the end, come through over time, and as we have noted before the residential market has been pretty immune from falls in at least nominal value.

In both UK and Europe valuations are now becoming more stable, and I would expect for the same reason they fell so fast, they will start to recover as rates fall.

For all that, in the equity market this year we have seen reasonable returns, as discounts to stated NAVs narrow, on both sides of the Atlantic. A number of activists are also pushing through mergers or reconstructions, which helps.

And yet nerves persist, the underlying discounts maybe less, but for Investment Trusts that own REITs, there are two tiers of discount (one underlying and one at the vehicle itself) and that top level has widened in cases.

Having endured that lot, and avoided earlier temptation, I am looking to re-stablish positions in half a dozen of these stocks in the UK and Europe, to work out the two that look like long term holds into the next cycle.

Not Renewed

Renewables have somewhat of the same issue, they are valued in part, again on the discount rate, so were driven down by rate rises, but also an odd view that energy prices are destined to fall over time. However, just as I have seldom seen prime city centre values fall for long, the hope of long run falling energy prices, runs counter to my experience.

There is also a great deal of uncertainty, both about what they produce, after numerous equipment and supplier failures, when they produce, and most of all, how to get product to the consumer with a credible margin.

But overall, the two sectors, property and renewables are quite similar, you have to get land, get planning, install infrastructure, hire builders, pay banks, realise your timescales were always far too optimistic, be nice to buyers, accept a discount, move on.

Having been wary of Renewables on the way down, I do now wonder if they are a separate asset class, or just a subset of several, including utilities, construction and distribution. If so, is it not better to leave that to the big multinationals with deep pockets?

Planting Tulips

So, to the new City Minister : Reading the current incumbent’s speech to the Stock Exchange, (not high on my list) it was of course indistinguishable from the last lot. The Treasury keeps these speeches, and the newest minister trots them out – often this is just an exercise in how well the next one mimics sincerity.

Has the Treasury orthodoxy changed? No. The allocation of capital remains the point of pain at the end of staggering amounts of hopelessly outdated regulation, some of them completely failing in their objectives. That much is unchanged.

Tulip herself is deeply worthy, UCL degree in Eng Lit, King’s London Masters in Politics, Policy, Government, so she should know how it all works and be able to write a good memo. But if we think the Government’s talk of “growth” is anything more than the illusory plug to stop the welfare budget draining us dry, a most implausible appointment. The milch cow must be kept placidly tethered, while it is milked.

The City will naturally be content, as ever, as long as no one rocks the boat.

But for all the ill-mannered sneering at the nice Mr. Draghi, and the EU’s failure to grow, we are in pretty much the same place. Now if Tulip wanted to be useful, and justify her principled disloyalty over leaving the EU, she should be mapping out how to join the Euro in 2030.

No road back to Rome exists, save through that thicket of joining the Euro first, the EU got that wrong before, it will not do so this time.

While of course half of Draghi’s capital market complaints are shorthand for saying that after all, Europe needs the City of London, not vice versa.

Cheer Up, They Said

After a pleasant summer, the dampness returns, exposing a quite enormous and unbalanced level of growth among the verdant thickets of both Middle England and the NASDAQ.

Markets must climb a wall of worry, and the next two months are not short of that. Forget interest rates and non-existent recessions, that’s just the stuttering voice of old economic models, fed fouled data from the last century.

IT IS ALL POLITICS

No, the risks now all look political; the prevailing orthodoxy is the West can keep borrowing levels high, to fund bloated and protected wages and welfare weirdness, impervious to international competition, or indeed to inflation. It has worked so far, and with excess and free flowing capital, there may always be a funder, mainly of state debt or residential mortgages, as well as a buyer of a few anointed equities.

And so far, that has remained the trend and indeed, somehow, the centre has held, once exceptional debt has now become permanent. This is aided in part by centre and centre left parties collaborating to silence the right, often behind the somewhat specious argument of protecting democracy from the wrong kind of votes.

But markets are jittery, they know the sums don’t add up, as do voters.

Debt as % of GDP, US in red, Japan in purple, UK light blue, France dark blue

IMF data mapper – from this page.

The same defence of democracy continues to require the now usual never-ending wars, and divisive and punitive trade barriers and sanctions.

Both businesses and investors are quite happy to sit on the sidelines, until a few questions get answered. The UK budget is expected to finally nail the myth of growth, by heavy new taxation, although it has almost been oversold, the reality might be a relief. It is not just the severity (it won’t be that bad) that matters, but also the direction of travel. Will it hammer savers, investors wealth creators and employment or attack consumption and waste?

Labour denials of an extra £2,000 a year tax on average incomes remains to us implausible and indeed we suggested many would be relieved at only that. Well before the election we said it will need about £20bn (economics is pretty simple really) and suggested the biggest chunk of that will come from fuel duties; we will see. Indeed, we’ve always known that various fudges would be used to skirt round the creaking OBR defences too.

The main UK stock market indices are once more in slow retreat, and while sterling is strong, we attribute that to short term interest rate differentials. High government borrowing is after all good for lenders. While in the US, it remains impossible to tell where the legislature ends up. Although like Starmer, many voters are so convinced the alternative is useless, they will overlook the socialist taint.

EMBRACING THE SIDELINES

Just now, the sidelines feel a good place: hedge funds, shortish term, high quality debt. There is scant evidence that the normal run upwards for emerging markets and smaller companies, from rate cuts, with attendant dollar weakness, has started, although many areas have moved in anticipation. But why buy in September when November is so much more certain?

That switch to smaller companies and emerging markets also may not happen this time, emerging markets have a lot of china dogs that look quite fragile, and smaller company liquidity is dire, so if yields stay high and defaults low, why add risk? While the inevitable fiscal squeeze will not help the hoped for returns and dynamism of a monetary easing cycle; you need both to work.

India meanwhile still stands out long term, but both the centre and more starkly the states are showing a notable loss of fiscal discipline, unrest in Bengal does not help and the IPO market is frothier than a Bollywood musical.

ROULETTE AT THE TORY PARTY

Given the apparent penchant for gambling, how many of the six (now five) chambers hold live rounds? We should glance at these ever-fascinating trials. The party faces strategic questions. Notably when does it expect to recover the 200 odd seats it needs, and how?

Well, I suspect the group saying next time (2029) will still dominate, although it looks rather unlikely. As to how, the assumption, I assume, is by halving the Lib Dems, but that’s only 36 seats, which leaves over 150 to get from Labour.

Interestingly every leadership candidate agrees that it was all Central Office’s fault, not for instance the wrong policies or a foolish rush to the polls. Most also at least pay lip service to rebuilding from the bottom up through local councils. Indeed, they even accept associations might matter.

Although there is also quite a bit, still, of finger crossing and waiting for Labour to implode. Not such an obvious solution this time.

As for Reform, if they also fail to implode, but settle in to be a real alternative, like their French and German counterparts, they will at least deny the Tory party their votes. Who knows, David Cameron might even emerge, in twenty years’ time, like Barnier as the compromise leader, from a party of no current electoral relevance.

It is hard to get involved in the contest, which will be down to four from the original six by next week. With so few MP’s, the choice is not brilliant.

It is a very narrow electorate, just 120 survivors of the wreck, so calling it and the shifting allegiances it reveals is hard. However once decided, it will be clear if the party is going long or short and which seats it is targeting, which in time will matter a great deal. Is it still unaware that a missed target could be fatal?

SAVERS TO BORROWERS

As for markets, I tend to ignore summer and short week trading, and the switch from bonds to equities, from savers to borrowers is a powerful economic force, as rates fall, but while the direction is clear, the angle of descent is not.

I assume it could be worse, that is even more uncertain but wondering how. Roll on Guy Fawkes Day.

OUR OWN EVOLUTION

This blog is evolving - when we started Monogram was a fund manager in widely accessible products, but that’s no longer the path - we are increasingly moving towards family offices and offshore clients.

With a less domestic focus, it seems time to move this to a stand-alone blog. Which brings with it a touch more freedom. It will continue to remain fascinated by the world of economics and politics, and indeed fund management. But may be happier to poke about in the mud for sustenance, or sound a startled alarm, as we become the Campden Snipe.

Blowing through the Jasmine

What is happening in the offshore wind market? Come to that what is happening in the onshore hurricane blowing round Westminster? And even after this market rally, arriving much as we expected last time, what should we still worry about? Valuations, recessions and inflation, all matter even if rate rises don't now.

A Feeling of Unreality in Westminster

One year in, Rishi looks incompetent and chaotically inconsistent. I simply can't explain Cameron's grinning re-emergence, it feels like a bad dream or worse joke. I hope he could never be selected again as an MP, after his murky financial dealings. The House of Lords is clearly less constrained. The arrogant indifference and heavy taint of sleaze can't be in the interest of voters.

There is a feel of an echo chamber inside Downing Street, of a puppet leader being strung along by unseen forces. Just last month the whole theme of the Party Conference was a fresh start, the last thirty years were apparently rubbish. Then we have this.

To the country and investors, it does not matter, although a half-awake opposition, or slew of oppositions, will be desirable in future; even if opposition politics is now easiest if you just wait for the other side to foul up and social media to rip them apart.

Zero-carbon? Can't Do it Yesterday?

A lot of notable recent shifts in the offshore wind sector, not surprisingly, as with so many zero carbon panaceas and the rush to do it all yesterday, the wheels are starting to come off. It is nothing like as cheap, or job creating, as the green zealots claimed or hoped. Protectionism is not helping either.

As Platts shows, for September, the more you make, the lower the price, just like real farming. UK offshore wind power is the least desirable in the entire European market.

Nothing wrong with the idea of offshore wind, and experts like SSE in the UK do well on big arrays in shallow waters, planned slowly, at least so far. Although even those are pricey and tend to need massive connecting grid structures.

Both Siemens and Orsted, to a degree newer entrants (at least compared to SSE), have taken a battering. Siemens had acquired a Spanish maker, but during the COVID fall out something came adrift, and it has hit big capacity and quality problems, resulting in billions in write offs – now it is restructuring – with a € 7BN subsidy from a group of banks. Heavy rotating machinery is always engineering hell; sticking it up a windy pole in salt water, is never that wise.

Orsted, the Danish developer, lopped 50% off its share price after ditching projects off Rhode Island and New Jersey - further billions written off. The idea you can put these things up off rocky coasts in areas of strong ocean currents and loads of shipping is quite interesting (and very New York, form over substance).

What torpedoed those projects was funding. The political desire for easy answers to high energy consumption made for poor outcomes (as ever), if everyone rushes to do it all at once, you simply create a cost bubble.

The single unit cost is never the same as for a thousand units; scaling up is always the tough part of any new technology.

Orsted share price - sourced from Yahoo finance - sharp focus on data

So, while Xi and Biden proclaim they will still save the planet, Biden rhetoric meets cost inflation once again, and cost inflation (and higher energy prices, a speciality of his) wins. Toss in protectionism, so that a Danish company is disqualified from his WTO busting subsidies, and the numbers no longer worked.

The Germans meanwhile find their own green funding trick ruled out by their own Constitutional Court, it involved taking a pre COVID funds surplus, and applying COVID emergency rules (on excessive deficit funding) and then spending it all post COVID. Isn't it odd that didn't really work? All three parts seem wrong.

Finally, the UK got no takers for this year's wind farm licences, as the guaranteed power price was too low. Next year the price has shot up, again guaranteeing higher energy prices for UK consumers (and industry) in the process.

Recession, Inflation and Valuations

Of the trio of recession, inflation and valuation, each investor has a particular fear. To me the nasty one remains inflation, and its friend rationing and stagnation. A lot simply can no longer be done. So that the modern solution (see above) of just throwing more money at it, from higher taxation and debt is largely pointless. Indeed, any farmer knows if you quadruple the inputs, it is still quite easy to halve the outputs.

We are deep into public service rationing now; we don't call it that, but persistent planned under delivery is rationing.

So, service sector inflation with declining 'outputs', is the issue. And that's the funny number 'outputs' we still record in GDP, so turning up, and being paid is an output, even if nothing (increasingly the case, both on turning up and doing anything) is actually done.

Recession? Well, I guess so, basic logic still says it must arrive some time; yet I still don't see big credit defaults or strain and a cooling labour market is clearly beneficial anyway.

And finally, valuations, well nearly everything looks cheap, outside big cap tech in the US, which somehow always feels pricey.

As rates fall through 2024, and funds flow out of cash and fixed interest, and M&A picks up, valuations still appear attractive. Albeit 2024 will (once more) be politically rather interesting.

Still, we could end up with some big questions answered and indeed big characters finally, finally, leaving the stage.

Maybe a summer breeze does lie ahead.

Charles Gillams

19-11-23

Stop Making Sense

The benign Powell’s fireside chat has left us all very happy, while I have been pondering the Yanis Varoufakis saga from afar. So how did Greece survive the doom and gloom after the Euro crisis?

An apposite topic, as high state debt, unproductive spending, and uncertain or burdensome credit, pretty much all over the West, apparently beckons once more.

The Song of Chairman Powell

We start with Chairman Powell in his recent Q&A: he could hardly have been nicer, the equity markets loved him, the bond markets sweetly retreated, and the dollar fell away.

It was not so much the repetition of ‘data dependent’, a seemingly meaningless phrase, or the deft swerves around repeated questions about the path of rates.

It was more the extra lengths he went to, to dismiss the data outliers, particularly on much faster GDP growth (4.9%) in the US economy, for Q3 and the sharp upward shift in longer term inflation expectations. The bond markets had found both metrics spooky.

The GDP number was dismissed, rather airily, as related to strong consumption, which in turn was linked to high employment and rising real wages on the one side, but more importantly to COVID savings balances. Although he admitted no one really knew what these were, but somehow, they were still contributing.

The inflation expectations got dissed even faster: Powell thought it an outlier, more recent data was far more consistent. Suddenly the evil portents were gone.

It would be wrong to think he knows what he is talking about (why start now?) but right, to know how he is feeling; that’s it. Sure, he keeps the rate rise out in the open, like an old dog, but the chain is lax and rusted, the beast benign.

It would take a lot to make the US raise rates again and he was happy with tighter monetary policies. Even nicer for the long end, while Powell is not sure where the “neutral” funds rate was (who is?), it was certainly a lot lower than where we are now. You might even choose to quantify a gesture; I’d say his was in the 3% area.

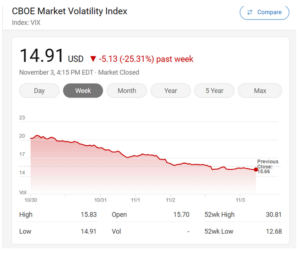

So, I feel like crisis-driven prices should not really apply. While the VIX? Down 25% in five days. Game over?

Search Results from MSN

Yanis, Right or Wrong?

Politically Yanis got lured by the old trap of supporting a party without a history, after sudden promotion, as a technocrat.

A rookie error.

But how does History see the Global Financial Crisis?

I looked at GDP from 2007 to 2022, for Bulgaria, Greece, France, Germany, UK, and the US. Here is the World Bank Chart of GDP growth rates. You can see Greece tumble out of the bundle, but it was also gathered back in, quite fast.

By 2007 the Eurozone was apparently out of control, spending was too high, it needed debt write downs, balanced budgets, selective privatisations and a war on tax evasion.

And Yanis felt Greece was being unfairly picked on to trial that medicine.

Size Counts

So, it is perhaps more instructive to look at levels, not growth rates. Here the damage is clearer, Greece has a GDP still substantially below the 2006 level. Bulgaria a neighbouring Balkan state, has doubled (and more) in the time. So Yanis has a point there.

Elsewhere France grew a shade faster than the UK, but from a slightly smaller base, so really little change.

But the US added almost twelve trillion dollars to its economy, which is like bolting on a new economy the size of the UK, France, Germany and Italy in just two decades.

We could adjust for currencies, population, different data points, calculation bases, of course and it is non-linear, inevitably. But we are looking big picture here.

Was The Left Right?

Gordon Brown was quite keen on the Yanis theory, and to some extent that adoration survived the subsequent dilettante Tory rule. Seizing big banks, attacking tax evasion at any cost, and aiming to balance budgets (Yanis was big on the primary surplus then) all crept into UK policy. The first two are oddly very non-Tory, especially when used to destroy economic growth by over-regulation. The third is quite sensible by comparison, but it was ignored.

Greece has since taken its medicine, with a steady swing to the Centre Right. Yanis finally lost his seat (for his new party) early this summer.

If the pain was indeed all inflicted to help the struggling IMF, no one told the US. If it was all done to save the Euro, I ask myself why did France go nowhere fast? It didn’t obviously hurt other Eastern European countries.

So, Greece remains an outlier, vastly reduced in wealth by the whole episode. It saved the Euro; it did not save Greece.

Where Next?

In the end, all national budgets work better with a growing economy, and in the long term that is essential. Flat or declining economies are the real crisis, especially without flat or declining state spending.

My highly selective period – (2007 being the pre-crash high) finds considerable upsides in both Trump and Biden’s expansion and in Obama’s reconstruction.

While if you need to know why the US stock market dominates in that period after the GFC, it is because GDP growth was twice that of Germany, and on course to double from 2007 quite soon.

Elephants can’t dance, they say, but when they do, the world shakes.

Insert Media here

Although Yanis, indeed has stopped making sense.

Charles Gillams

4.11.23