Cheer Up, They Said

After a pleasant summer, the dampness returns, exposing a quite enormous and unbalanced level of growth among the verdant thickets of both Middle England and the NASDAQ.

Markets must climb a wall of worry, and the next two months are not short of that. Forget interest rates and non-existent recessions, that’s just the stuttering voice of old economic models, fed fouled data from the last century.

IT IS ALL POLITICS

No, the risks now all look political; the prevailing orthodoxy is the West can keep borrowing levels high, to fund bloated and protected wages and welfare weirdness, impervious to international competition, or indeed to inflation. It has worked so far, and with excess and free flowing capital, there may always be a funder, mainly of state debt or residential mortgages, as well as a buyer of a few anointed equities.

And so far, that has remained the trend and indeed, somehow, the centre has held, once exceptional debt has now become permanent. This is aided in part by centre and centre left parties collaborating to silence the right, often behind the somewhat specious argument of protecting democracy from the wrong kind of votes.

But markets are jittery, they know the sums don’t add up, as do voters.

Debt as % of GDP, US in red, Japan in purple, UK light blue, France dark blue

IMF data mapper – from this page.

The same defence of democracy continues to require the now usual never-ending wars, and divisive and punitive trade barriers and sanctions.

Both businesses and investors are quite happy to sit on the sidelines, until a few questions get answered. The UK budget is expected to finally nail the myth of growth, by heavy new taxation, although it has almost been oversold, the reality might be a relief. It is not just the severity (it won’t be that bad) that matters, but also the direction of travel. Will it hammer savers, investors wealth creators and employment or attack consumption and waste?

Labour denials of an extra £2,000 a year tax on average incomes remains to us implausible and indeed we suggested many would be relieved at only that. Well before the election we said it will need about £20bn (economics is pretty simple really) and suggested the biggest chunk of that will come from fuel duties; we will see. Indeed, we’ve always known that various fudges would be used to skirt round the creaking OBR defences too.

The main UK stock market indices are once more in slow retreat, and while sterling is strong, we attribute that to short term interest rate differentials. High government borrowing is after all good for lenders. While in the US, it remains impossible to tell where the legislature ends up. Although like Starmer, many voters are so convinced the alternative is useless, they will overlook the socialist taint.

EMBRACING THE SIDELINES

Just now, the sidelines feel a good place: hedge funds, shortish term, high quality debt. There is scant evidence that the normal run upwards for emerging markets and smaller companies, from rate cuts, with attendant dollar weakness, has started, although many areas have moved in anticipation. But why buy in September when November is so much more certain?

That switch to smaller companies and emerging markets also may not happen this time, emerging markets have a lot of china dogs that look quite fragile, and smaller company liquidity is dire, so if yields stay high and defaults low, why add risk? While the inevitable fiscal squeeze will not help the hoped for returns and dynamism of a monetary easing cycle; you need both to work.

India meanwhile still stands out long term, but both the centre and more starkly the states are showing a notable loss of fiscal discipline, unrest in Bengal does not help and the IPO market is frothier than a Bollywood musical.

ROULETTE AT THE TORY PARTY

Given the apparent penchant for gambling, how many of the six (now five) chambers hold live rounds? We should glance at these ever-fascinating trials. The party faces strategic questions. Notably when does it expect to recover the 200 odd seats it needs, and how?

Well, I suspect the group saying next time (2029) will still dominate, although it looks rather unlikely. As to how, the assumption, I assume, is by halving the Lib Dems, but that’s only 36 seats, which leaves over 150 to get from Labour.

Interestingly every leadership candidate agrees that it was all Central Office’s fault, not for instance the wrong policies or a foolish rush to the polls. Most also at least pay lip service to rebuilding from the bottom up through local councils. Indeed, they even accept associations might matter.

Although there is also quite a bit, still, of finger crossing and waiting for Labour to implode. Not such an obvious solution this time.

As for Reform, if they also fail to implode, but settle in to be a real alternative, like their French and German counterparts, they will at least deny the Tory party their votes. Who knows, David Cameron might even emerge, in twenty years’ time, like Barnier as the compromise leader, from a party of no current electoral relevance.

It is hard to get involved in the contest, which will be down to four from the original six by next week. With so few MP’s, the choice is not brilliant.

It is a very narrow electorate, just 120 survivors of the wreck, so calling it and the shifting allegiances it reveals is hard. However once decided, it will be clear if the party is going long or short and which seats it is targeting, which in time will matter a great deal. Is it still unaware that a missed target could be fatal?

SAVERS TO BORROWERS

As for markets, I tend to ignore summer and short week trading, and the switch from bonds to equities, from savers to borrowers is a powerful economic force, as rates fall, but while the direction is clear, the angle of descent is not.

I assume it could be worse, that is even more uncertain but wondering how. Roll on Guy Fawkes Day.

OUR OWN EVOLUTION

This blog is evolving - when we started Monogram was a fund manager in widely accessible products, but that’s no longer the path - we are increasingly moving towards family offices and offshore clients.

With a less domestic focus, it seems time to move this to a stand-alone blog. Which brings with it a touch more freedom. It will continue to remain fascinated by the world of economics and politics, and indeed fund management. But may be happier to poke about in the mud for sustenance, or sound a startled alarm, as we become the Campden Snipe.

Blowing through the Jasmine

What is happening in the offshore wind market? Come to that what is happening in the onshore hurricane blowing round Westminster? And even after this market rally, arriving much as we expected last time, what should we still worry about? Valuations, recessions and inflation, all matter even if rate rises don't now.

A Feeling of Unreality in Westminster

One year in, Rishi looks incompetent and chaotically inconsistent. I simply can't explain Cameron's grinning re-emergence, it feels like a bad dream or worse joke. I hope he could never be selected again as an MP, after his murky financial dealings. The House of Lords is clearly less constrained. The arrogant indifference and heavy taint of sleaze can't be in the interest of voters.

There is a feel of an echo chamber inside Downing Street, of a puppet leader being strung along by unseen forces. Just last month the whole theme of the Party Conference was a fresh start, the last thirty years were apparently rubbish. Then we have this.

To the country and investors, it does not matter, although a half-awake opposition, or slew of oppositions, will be desirable in future; even if opposition politics is now easiest if you just wait for the other side to foul up and social media to rip them apart.

Zero-carbon? Can't Do it Yesterday?

A lot of notable recent shifts in the offshore wind sector, not surprisingly, as with so many zero carbon panaceas and the rush to do it all yesterday, the wheels are starting to come off. It is nothing like as cheap, or job creating, as the green zealots claimed or hoped. Protectionism is not helping either.

As Platts shows, for September, the more you make, the lower the price, just like real farming. UK offshore wind power is the least desirable in the entire European market.

Nothing wrong with the idea of offshore wind, and experts like SSE in the UK do well on big arrays in shallow waters, planned slowly, at least so far. Although even those are pricey and tend to need massive connecting grid structures.

Both Siemens and Orsted, to a degree newer entrants (at least compared to SSE), have taken a battering. Siemens had acquired a Spanish maker, but during the COVID fall out something came adrift, and it has hit big capacity and quality problems, resulting in billions in write offs – now it is restructuring – with a € 7BN subsidy from a group of banks. Heavy rotating machinery is always engineering hell; sticking it up a windy pole in salt water, is never that wise.

Orsted, the Danish developer, lopped 50% off its share price after ditching projects off Rhode Island and New Jersey - further billions written off. The idea you can put these things up off rocky coasts in areas of strong ocean currents and loads of shipping is quite interesting (and very New York, form over substance).

What torpedoed those projects was funding. The political desire for easy answers to high energy consumption made for poor outcomes (as ever), if everyone rushes to do it all at once, you simply create a cost bubble.

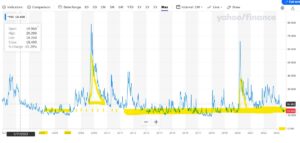

The single unit cost is never the same as for a thousand units; scaling up is always the tough part of any new technology.

Orsted share price - sourced from Yahoo finance - sharp focus on data

So, while Xi and Biden proclaim they will still save the planet, Biden rhetoric meets cost inflation once again, and cost inflation (and higher energy prices, a speciality of his) wins. Toss in protectionism, so that a Danish company is disqualified from his WTO busting subsidies, and the numbers no longer worked.

The Germans meanwhile find their own green funding trick ruled out by their own Constitutional Court, it involved taking a pre COVID funds surplus, and applying COVID emergency rules (on excessive deficit funding) and then spending it all post COVID. Isn't it odd that didn't really work? All three parts seem wrong.

Finally, the UK got no takers for this year's wind farm licences, as the guaranteed power price was too low. Next year the price has shot up, again guaranteeing higher energy prices for UK consumers (and industry) in the process.

Recession, Inflation and Valuations

Of the trio of recession, inflation and valuation, each investor has a particular fear. To me the nasty one remains inflation, and its friend rationing and stagnation. A lot simply can no longer be done. So that the modern solution (see above) of just throwing more money at it, from higher taxation and debt is largely pointless. Indeed, any farmer knows if you quadruple the inputs, it is still quite easy to halve the outputs.

We are deep into public service rationing now; we don't call it that, but persistent planned under delivery is rationing.

So, service sector inflation with declining 'outputs', is the issue. And that's the funny number 'outputs' we still record in GDP, so turning up, and being paid is an output, even if nothing (increasingly the case, both on turning up and doing anything) is actually done.

Recession? Well, I guess so, basic logic still says it must arrive some time; yet I still don't see big credit defaults or strain and a cooling labour market is clearly beneficial anyway.

And finally, valuations, well nearly everything looks cheap, outside big cap tech in the US, which somehow always feels pricey.

As rates fall through 2024, and funds flow out of cash and fixed interest, and M&A picks up, valuations still appear attractive. Albeit 2024 will (once more) be politically rather interesting.

Still, we could end up with some big questions answered and indeed big characters finally, finally, leaving the stage.

Maybe a summer breeze does lie ahead.

Charles Gillams

19-11-23

Reserve in Reverse

Fallen Emperor?

With almost two thirds of global equity markets represented by the US, the fall in the dollar so far this year is quite dramatic, and for many investments, more important than the underlying asset.

UK retail investors are especially exposed to this, as although Jeremy Hunt (UK Chancellor) may not notice it, the US is where most UK investors went, when his party’s policies ensured the twenty-year stagnation in UK equity prices.

While Sunak continues to pump up wage inflation, which he claims, “won’t cause inflation, raise taxes or increase borrowings” Has he ever sounded more transparently daft? Sterling, knowing bare faced lies well enough, then simply drifts higher. Markets know such folly in wage negotiation can only lead to inflation and higher interest rates.

We noted back in the spring, in our reference to “dollar danger” that this trade (sell dollar, buy sterling) had started to matter, and we began looking for those hedged options, and to reduce dollar exposure. To a degree this turned out to be the right call, but in reality, the rate of climb of the NASDAQ, far exceeded the rate of the fall in the dollar.

While sadly the other way round, a lot of resource and energy positions fell because of weaker demand and the extra supply and stockpile drawdowns, which high prices will always produce. But that decline was then amplified by the falling dollar, as most commodities are priced in dollars. So, a lot of ‘safe’ havens (with high yields) turn out to have been unsafe again.

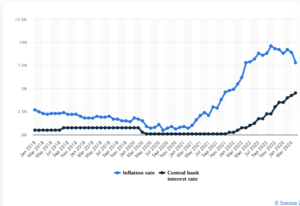

The impact of currency on inflation

Currency also has inflation impacts. Traditionally if the pound strengthens by 20%, then UK input prices fall 20%. The latest twelve-month range is from USD1.03 to USD1.31 now, a 28% rise in sterling.

In a lot of the inflation data, this is amplified by a similar 30% fall in energy, from $116 to $74 a barrel for crude over a year. In short, a massive reversal in the double price shock of last year. In fairness this is what Sunak had been banking on, and why the ‘greedflation’ meme is able to spread. But while that effect is indeed there, other policy errors clearly override and mask it.

A Barrier to the Fed.

In the US we expect the converse, rising inflation from the falling currency, maybe that is creeping through, but not identified as such, just yet, as price falls from supply chains clearing lead the way, but it is in there.

Finally, of course, this time, the dire performance of the FTSE is probably related to the same FX effect on overseas earnings assumptions. Plus, the odd mix of forecast data and historic numbers that we see increasingly and idiosyncratically used just in the UK. If the banks forecast a recession, regardless of that recession’s absence, they will raise loan loss reserves, and cut profits, even if the reserves never get used.

Meanwhile, UK property companies are now doing the same, valuing collapsing asset values on the basis of the expected recession, and not on actual trades. So, if you have an index with heavy exposures to stocks, that half look back, half reflect forward fears, it will usually be cheaper than the one based on reality.

Why so Insipid?

OK, so why is the dollar weak? Well, if we knew that, we would be FX traders. But funk and the Fed’s ‘front foot’ posture are the best answers we have, and both seem likely to be transient too.

If the world is saying don’t buy dollars, either from fear of the pandemic or Russian tank attacks or bank failures, that’s the funk. As confidence resumes and US equity valuations look more grotesque, the sheep venture further up the hill and out to sea. To buy in Europe or Japan, they must sell dollars.

The VIX, in case you were not watching, has Smaug like, resumed its long-tailed slumber, amidst a pile of lucre.

From Yahoo Finance CBOE Volatility Index

So as the four horsemen head back to the stables, the dollar suffers a loss.

The Fed was also into inflation fighting early; it revived the moribund bond markets, enticed European savers with positive nominal rates, (a pretty low-down trick, to grab market share) and announced the end of collective regal garment denial policies. But having started and then had muscular policies, it must end sooner, and perhaps at a lower level. So that too leads to a sell off in the dollar.

Where do we go instead?

So where do investors go instead?

In general, it is either to corporate debt, or other sovereigns. Japan is not playing, the Euro maybe fun, but not so much if Germany is getting back to normal sanity and balancing the books again. So, the cluster of highly indebted Western European issuers are next.

Sterling now ticks those boxes, plenty of debt, liquid market, no fear of rate cuts for a while, irresponsible borrowing, what is not to like?

For How Long

When does that end? Well, the funk has ended. You can see how the SVB failure caused a dip in the spring, but now the curve looks upward again. Although fear can come back at any time, as could some good news for the UK on inflation. However even the sharp drop the energy/exchange rate effects will cause soon, leave UK base rates well south of UK inflation rates.

So, every bit of good news for the Fed, is bad news if you hold US stocks here.

How high and how fast does sterling go?

Well, it has a bit of a tailwind, moves like any other market in fits and starts, but could well go a bit more in our view. Oddly the FTSE would be a hedge (of sorts).

It is Not a Pipe

A long view this time : Has the price of capital changed for good? How bad is the UK position? Oh, and the unusual universality of colonialism.

A Far Off Galaxy

Let’s start with colonialism. I have been reading about the benighted past of Bulgaria (R.J. Crampton, 2nd Ed, CUP). A Bulgarian I know said that the country ‘has a knack for picking the wrong side’ - a little harsh, I thought. However, it has always existed as a colony, aside from a brief imperial phase around the last millennium but one, and before that when it equated to Thrace, almost as far back again.

Given the option, Bulgaria recently opted to join the Western European empires’ current formulation as the EU and NATO - the latter being the armed wing of Western thought. Bulgaria had suffered horribly under the Soviets, with a steady and ruthless coercion of an existing multiparty democracy, at a speed just enough to keep outsiders ignorant, or if not, passive.

That history gives me a whole new viewpoint, on the string of broadly similar states. The Balkans and The Middle East all appear in a new light, and indeed I start to comprehend the bitter sideshows (as they seem now) in both World Wars, over that same terrain.

The collapsing empires (Russian, Ottoman, Roman,) seem more influential than the current rulers in so many former colonial states. They are really not, as we think now, a series of nations fighting for ‘independence’. In most cases that independence is fragile to the point of being mythical, while the internal fissures are enduring. The cracks of nations within empires, not of states within a world.

Now You See It

One passage in Crampton’s work stood out “by mid-summer social and industrial unrest were widespread with strikes by civil servants. On transport networks, and despite the provisions of the law, in the ports and medical services. The government was forced to grant a 26% wage increase to all state employees, an action which weakened its attempts to control the budget deficit and inflation and which did little to impress the international financial organisations.”

Written about conditions just before another wrenching Balkan realignment last century, this rather made me stop and reflect.

A parallel with the UK?

Just how close are we in the UK to that edge? Lost in a warm feeling for individual strikers and their causes, and a very British willingness just to plough on, there still seems to be a real danger.

I am well aware of our great national strengths, in the arts, our language, higher education, science, heritage, even logistics and retailing - they are enduring causes for optimism. But long-term investors need to weigh up the recent damage, especially the loss of political capital by the “responsible” right, the high levels of debt and taxation, which coupled with low productivity, could also spell trouble, the certainty of ongoing nationalism and the unhealed rift of Brexit.

There is danger too in the probability of a Labour government, which however centrist the leader is, will have left wing factions to assuage. It is equally dangerous to continue our recent experience of minimal ministerial experience. I hope the change won’t be as bad as I fear, but it will probably be worse than I hope.

This remains a reason for the FTSE to be anchored to late 20th Century levels, despite almost every stock I research looking cheap. The fear of being still cheaper tomorrow rules.

Do Markets Care?

On the other hand, re-pricing capitalism after the decade of populist nonsense by central bankers does feel pretty good. If you have no cost of money and no reward for savers, financial gambling prevails.

All of this raises a key issue: is the apparent resurgence of speculation (the greater fool theory of investing) permanent? In which case investors should probably just watch momentum. Or is this most recent re-run of the last decade’s speculative phase, really transient?

For a better view, see this page on Statista

As long as inflation exceeds the cost of money, assets will likely rise; the widespread return of real interest rates (a point we are almost at) should slow that down.

After that point what matters is cash flow, and whereas gambling will favour growth stocks, real returns come about when interest rates are high, but inflation is also falling. The gap matters and we are not there yet.

This is probably the crux of the next two years, and we doubt that having had a serene and slow drift towards recession, there is any reason either to expect a suddenly faster descent now, or really to expect the corollary, a sudden fall in interest rates, to offset a deep recession.

If rates stay high, but have indeed peaked and inflation declines, value investors should be in a better place. If they get it wrong, they are at least paid to wait.

As we have seen in the last twelve months, growth investors fuelled by borrowed money really do need a rising market, they get hit twice if it falls: both through a loss of capital and then the need to fund loss-making assets at real rates.

The Monogram View

Overall, our position has been that fundamentals should win, but we suspect momentum will win. Spotting the next momentum shift early, therefore remains a powerful driver of returns.

One narrative of 2023 (so far) is that the SVB crisis and stronger growth combined led to far more liquidity than markets expected. This fed into the gambling stocks, giving them momentum.

So, although the first half was not what we expected, the second half might still be. But it is just one narrative, and it may still be the wrong one.

Note : Further reading, for those interested in Bulgaria :

See also, The Bogomils: A Study in Balkan Neo-Manichaeism, Obolensky, Dmitri.

Skipping along

Skipping is the week’s theme, following the inadvertent use of the term by the Fed Chairman, along with the rather weird behaviour of Jeremy Hunt.

Although any skipping seems unlikely soon, on this side of the Atlantic.

The dear old ‘recession’ still lingers, unseen but feared, like an ex Prime Minister. We are convinced it will arrive, but as a ‘technical’ recession only. It should be hard for anyone to be surprised. Labour markets are much stickier and far more fragmented. Supply is short, so any systemic shock feels unlikely. While as old hands keep noting, single figure mortgage rates, well below inflation rates, are hardly restrictive.

Chair Powell (almost) mentions ‘skipping’.

Jerome Powell was bowling along contentedly, when he suddenly described the Reserve Board’s June inactivity as ‘skipping’. Although it actually was just a ‘skip’, before he realised the error and with a guilty look speedily reverted to the far more passive ‘pausing’. But we knew how he was thinking. He was going to keep his foot on the neck of borrowers for a bit longer – interestingly, he refers to real rates of interest, as somehow unjust and injurious. Odd that when asked anything about fiscal policy he instantly plays the neutral, technical banker, no good and evil there.

Moves in the real economy.

So, what has really happened?

Not a lot, energy prices have climbed all the way up, and now slid all the way down. Aggressive fiscal stimulus continues, any chance Biden has to bribe the electorate with their own money, he still takes. Employment remains strong, although there is some tightening in hours worked, but it is still pretty hard to see how the Fed gets down to 2% inflation for a year or two.

And yet, markets by a mix of that unseen recession and faith in so called base effects, do think inflation by the autumn, will justify a real pause. No skipping.

UK Chancellor’s odd statements

Here in the UK Jeremy Hunt is in quite a different place. Inflation still looks high and embedded, but he has carefully outlined how he would keep going with substantial hand outs to offset inflation (aka fiscal stimulus).

However, inflation control was all for the Bank to sort out.

This is nonsense, of course. The UK Government is yet again stoking inflation while taking no responsibility for stopping it. He then gave a tortuous explanation as to why his policies have now produced exactly the same interest rates as the Truss typhoon, created by his reckless predecessor, but somehow, not at all the same.

Rate rises – a global feature.

Funny that, as we noted at the time, there was little odd about the October rate spike, and much that the Bank could have done (but refused to) by a prompt rate rise (matching the US) to stabilise the currency and inflation.

Rate rises are a global feature, with not a lot one small country could do about it.

2021 chart produced by the UK Institute of Chartered Accountants

So quite where the virtue of the Truss toppling quarter point rise is now, is rather unclear.

As sterling shows, the prize for that autumnal sloth will be higher rates (and inflation) than elsewhere for longer. The thing about fire fighting is the sooner you start the less you have to do.

So how did Monogram’s methodology work?

Our in-house model switched into Japan in December 2022 and Europe in March 2023. As we only ever deal in half a dozen big global index Exchange Traded Funds, this is not a tickle, but 25% of the total equity position in (or out) at once.

Brutal and scary, but effective.

We look at the signal, kick the tyres, thump the bonnet, turn it off and on again, look for reasons to ignore it, and then six months later look back in wonder and say, “oh yes, that was right”. These signals are delicate enough to very seldom feel right at the time, but after almost a decade of running the model, we have learnt to obey.

So, our Momentum performance discussion, yet again, is about how much we made, not about in which direction the money went. While the GBP version, seeing similar signals, has also never come out of the S&P 500, which for a good while also felt wrong, but it seems was right, taking a long view. The USD model was more skittish but is back in both (S&P and NASDAQ) US indices now.

So, we do know where momentum has been, and it is quite strong.

Markets in the political timeline

The rational thinkers say the market is (still) too expensive, but the trend followers don’t agree, who is right?

We tend to feel just as Central Bankers were very slow to spot inflation, they are possibly being too slow to see it has now been contained, and the US skip may be a pause and then a snooze. Which would be very convenient for the Fed during the US Primaries, allowing for cuts into the US election?

Related to that, we watch with amusement a dialogue about the attractiveness of stock exchanges, in particular in London, couched entirely in terms of what potential listing companies say they want. Not a mention of what investors want, as if they just don’t matter. Quite absurd, as what all listings need is a deep market, good liquidity, stable tax regimes, and an attractive base currency.

Is London aiming to provide these? We seem to favour founders – so, tweaks to voting rights, smaller free floats, fewer shareholder rights. But then oops! No buyers.

This is worse than nonsense, it damages what little is left of London’s reputation. In this market you start with the buyers. The price performance of many a recent IPO spells out the problem, the sellers are finding it too easy to deceive people – a call is needed for greater transparency, longer lock-ins, and less pandering to insiders and their advisers (not more).