Small Earthquake

Full year corporate accounts have now all been published, in several cases even read, so it is time to look at the raw data beneath all those clever funds and derivatives, at the underlying companies.

There are two themes emerging: one is the extraordinary scale of movements last year in defined benefit pension assets and liabilities, and the other is how we should evaluate the size of the Scottish discount.

Pension Asteroids Collide

Enormous numbers are shifting on defined benefit pension schemes, nearly all the big ones seeing asset losses of several billion, but with matched declines in liabilities of the same scale, leaving almost no apparent change, all stitched back together. This impacts in particular the big banks, utilities, resource majors and of course life companies.

It is a source of some nervousness, when large numbers crash about the balance sheet, dwarfing the trivial numbers in the profit and loss account. But they are also quite different items, the asset declines (from long dated gilts) are real money, stuff you could have woken up at the start of the year, picked up a phone and sold.

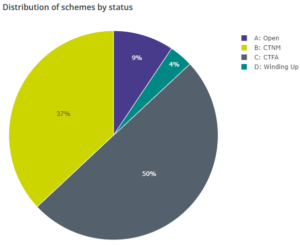

Yet the liabilities in terms of actual money to retirees hardly shifted, it was just discounted differently. While nearly all (91%) of the 5,000 odd UK schemes are either Closed To new members (CTNM) or to future accruals (CTFA). So, of little current relevance to operations.

From: This page on the UK Regulator’s website – the key to the abbreviations is also there.

What is relevant is the sudden loss of tens of billions of pounds ny these pension funds. But that is ignored, because of the liability offset, but it was lost and is gone. This came along with dramatic changes in the value of the gilts they hold, in cases by more than the unit value decline, as gilts were actually being sold quite hard too - a big chunk of assets that no longer exists.

Scottish Exceptionalism

So, to the Scottish discount. What is it? In our valuation models we discount earnings for political and operational risks, including for governance, including the location of the auditors. It is an internal assessment, so matters not a jot, unless others do the same.

We know the discount exists, the reversing tide of “swimmers” or companies raising money outside their domestic market, tells you the entire UK is already at a fair old discount to the US, even for companies with mainly US earnings. Should the same apply to Scotland? And by how much more? 20%? Whatever it is, it is getting bigger for us.

In my view if you are a FTSE100 Company, you have big four auditors, London office. Regional offices and smaller firms will be more dependent on a single big client and in enough cases to matter, that disproportionate power will swing it, for the Board, against the investors. Not that London based Big 4 is perfect (we know they are not).

So, to Scotland, there is a long-standing assumption they will use Scottish audit offices, and a drift to using Scottish firms too. This used to mean high quality, but I now sense they lack experience. Boards have also increasingly become reliant on a smaller pool of candidates, and two recent high-profile cases leave me wondering about their governance.

1. Scottish Mortgage Investment Trust

We sounded the alarm on the peculiarities of this popular fund two years or so ago, in their glory days. Like some other troubled funds, they took on more and more unquoted holdings. All disclosed and approved, but in the end clearly linking private and public markets, indeed boasting of how many of their quoted holdings started out as private ones. Well, a closed IPO market knocks that bet pretty hard. When a lot of them are also Chinese, that renders that pipeline even more suspect.

While disclosed, yes, but adequately disclosed? In one case they hold G, I, H, A, C, B Prefs and A Common Stock, with greatly varying valuations by class. We were nervous, when the share price failed to discount these holdings, at a time when other equity trusts, indeed private equity specialists, were facing growing discounts on their holdings.

That has now corrected, the Board has finally stood up to the manager and questioned the existence of the in-house skills to back up these valuations. But in the process our Scottish discount opened up.

From a three year high of over £14 per share, SMIT has fallen hard to just over £6, wiping out half the value or the thick end of £10bn, from presumably mainly UK retail holders. It has kept falling. I think it will need to list those unquoteds separately, and give holders a share in each asset pool, to regain its once illustrious crown.

2. John Wood Group

The John Wood Group, which operates in natural resource consulting and contracting, has been a disastrous investment. A well-respected consulting firm, its Board decided to merge with another well-respected quoted consulting firm, Amec: outcome? Hugely negative. Five years ago, its shares were over £5 and even quite recently shareholders were hoping a private equity bid would rescue them after only a 50% loss.

But having overseen that catastrophe, the Board seemed not to be listening. They only very reluctantly agreed to bid talks, and somewhere in those talks something persuaded the bidder to back off. From the bid inspired high of £2.55, it has now virtually halved again. The Board feels old style, out of date, insular. I particularly enjoyed (it is one of the few pleasures of reading so much verbiage) their illustration for the diversity report, (see below).

Extracted via screenshot from the Annual Report and Accounts of the John Wood Group

This reminded me of sitting on a School Curriculum Committee (see the fun I have). We had to cover multiculturism, and the teacher (in the high pale Cotswolds) chose India; intrigued I asked why? The answer was that allowed the topic to be covered for our forthcoming Ofsted inspection, by having a takeaway meal in class. That was it. No map, no history, no people, just an affiliated consumable.

But nice money for the executives, look at last year’s bonus structure. That odd picture served them well. For an original business that is now itself worth nothing and half of what it paid for Amec !

Now, but for that Board, or that history, Wood looks a nice business, cleaned up, $5 billion of apparently profitable sales, with a market cap of £1 billion, not a lot of debt, all three divisions profitable at least at the EBITDA line. Heavily exposed to renewables, including in North America, it even reports in dollars. You could argue the bid was low - no doubt the Board did - but if the price then halves, after the bid vanishes, how credible are they?

So, in comes the Scottish discount – because this pattern of behaviour speaks of a particular culture and leaves me feeling the need for a bigger safety margin, to buy a business from that region.

Wood for the trees

We have all been obsessed with rates and inflation, but we seem to be in danger of missing what looks like a widespread bull market running broadly from last October. This is widely applicable outside the main US markets, including in gold. There is a similar and at times masking trend of dollar weakness.

What are the implications of this?

We also look at the unending tragedy of the various remnants of the Tory party.

Still Rising?

With markets still fixated on the next crash, we can sometimes overlook the long momentum swings. Although the US banking crisis matters, it is of little relevance to the far more concentrated and tightly controlled Basel III banks in Europe. Many would say to excess, but they are clearly tighter rules. The few assets not marked to market are a footnote in Europe; in the Wild West of US regionals, they can be the whole story.

On a one-year basis, the France CAC 40 is up 14%, the German DAX by 12%, with both the UK large cap and Japan’s Nikkei also positive, so equity markets have been strong, almost regardless of rate rises. The US is the main home of negative twelve month returns, but the gap between the S&P and the NASDAQ declines over that period, is now quite small, after the spring bounce back in the latter.

What does that mean?

For all the media love of the disaffected trashing their own communes, doing the right thing on pensions (they were very out of step) apparently helps France.

While the splitting of power in the US Congress and the meanderings of a senile President, has perhaps hurt the US, with everything from banking regulation to the debt ceiling made into a political game.

Brazil is down too, but India and Russia are up.

Well perhaps I go too far, but maybe there is a pattern? Markets like stability.

Relative values

While comparisons are complex where accounting systems diverge, the UK still looks like the lowest rated with the highest yield, and conversely the NASDAQ still has (by some way) the highest rating and lowest yield. US earnings are it seems still much more valuable.

The savagely anti-business stance of the UK, including a brutal rise in corporation tax maybe part of it, it will create a fall in earnings (and likely dividends) next year.

While the less visible, but still onerous onslaught in the US, including a minimum tax take, won’t be good.

So, does inflation matter?

The UK perhaps is also seen as the one major European market that looks to have dithered too long on controlling inflation (which could explain sterling strength). However, I see no real appetite for more austerity in the UK, so I find that assumption slightly puzzling. Having the FX market convinced UK rates are going a lot higher (because of policy failures) is hardly comfortable, but feels a little like re-living last year now.

Oddly too, controlling inflation the US way, has hurt equity markets more, it seems, than letting it burn out in the European style. Heresy to many of us, but that’s what the numbers imply.

All the theory, all the historic data says we now must get a sharp recession, but then grandpa, pray where is your beloved recession? Still looking, since mid February. It seems we must appease the inverted yield curve and believe base rates matter, but a bit more evidence would certainly help.

And rate cuts will be a powerful tonic, when they come. The bears are now reliant on widespread recessions, and soon.

Perhaps the best of this little bull market has gone, but there is a lot of liquidity still about and being out of the market with high inflation, is not great.

A multitude of sins – local elections coming up

And what of the UK Tory “Party”, if such a mess can be called that. The assumption for a while has been that the imminent local elections will be bad for them. However, they are a curious mix of voting locations this time, not London, not all of the Home Counties, none of the Celtic fringe, but a good chunk (but again not all) of the Red Wall seats. See map below.

Map from Wikipedia page on 2023 local elections

But really it is heavily biased to the Tory heartland, vast swathes of Labour free wards, where they are not even bothering with candidates, so it will not tell us that much. The Lib Dems will do well, but significant conquests in many areas will now require quite substantial swings.

The assumption is also that Dominic Raab was cut down by Sunak, who has yet to learn that throwing competent colleagues under the bus may feel good, but it thins the ranks of effective ministers, and builds up the malcontents. He has handled these badly, and forgets the real target is not his ministers, but his own position.

Tory strategy

Seemingly the Tory party has run just one electoral strategy for years, based on old victories; just trash the opponent. In a two-party state, voters must then decide who they dislike least. And both Labour (and the SNP) have reliably offered something so vile, that a simple victory follows.

But no longer, Labour (despite their recent rather crude posters) still seem innocuous.

The Lib Dems are sticking to their amateur politics, which can also look strangely alluring, if the other two parties look mysterious or inept. The Tories (like the SNP) are now in danger of being judged by results, not by fear or hatred of the alternative.

The score card on that basis looks pretty bad, and Sunak’s pledges are so far, going the wrong way.

The Scottish Play: Luck or judgement?

Three topics this week: has Sunak’s luck changed? Has India’s bull run ended, and where is this much-discussed recession?

The Art of the Possible

Image from Wikemedia - by Neide José Paixão

Looking at Absolute Return – Can it be Done?

A wise old hand once told me that all investors want is protection from inflation; do that, earn your fees and your job’s done. Read more

All Clear? REITs and Private Equity

When do we go back to property (REITs) and private equity (PE)? We look closely at these two areas, as there appears to be nothing new to see or say on interest rates or inflation.

Macro is dull just now

Neither the Fed nor the Bank of England, nor indeed the ECB meet this month. So, the default is to assume a half point rise all round. Which should mean Western central banks are broadly aligned for a while, so by implication are currencies.

Clipped from this site – downloadable from source.

Recessions lag rate rises, so are not due yet either, although clearly one is coming.

Inflation will probably drift lower, but the employment markets stay strong, as the shuddering readjustment out of COVID continues to keep churn elevated. In person service hires roughly balance stay-at-home sector losses for now.

Basic food commodities, which have driven much of the recent inflation surge, will stay elevated until the current crops/stock are harvested and replanted late in the spring. Energy is possibly oversupplied for this winter. So not that much change in those two inflation drivers yet.

REITs

So, when is it safe to go back into risky assets? We look at two contrasting stories, firstly REITS which are seen as bond proxies, so cannot properly bounce until rates top out. This seems to need a couple of months at “no change” from the Central Banks. We are less sure about quantitative tightening ending, but most of the market gets spooked by that too. We think it matters little, because masses of global liquidity make what US banks hold somewhat irrelevant.

Nor do we see why REIT assets held on 7–8-year leases with typical debt fixed for half that term, should oscillate so violently over a few months, but that’s life, they just do.

Does property matter?

Institutional interest is not high, we know that, and most institutions need daily liquidity before all else, which lumpy property can’t give. Plus, for boring old REITS a lot has changed for the worse.

Who knows where retail space settles? It remains over supplied (and overtaxed), likewise probably office space, with the added wrinkle of retrofitting for carbon neutrality. COVID created an excess of new storage and warehousing, which also needs to be worked through, so that’s not safe either. While no institution wants the grief (or bad publicity) of dealing with individual tenants and homeowners, so we have long thought if you want to play the residential market, buy high street banks, as a kind of proxy. Mortgage lending is about all they do now.

It is private investors who still love property as a tangible asset; most are over invested in property and have been over rewarded for being so. Habit really. But if they had that habit before, they are still keen to know when to step back in, at bargain basement prices.

Private equity

Now PE, is a bit different. Yes, private investors like it (like hedge funds) but trust it about as much. Never sure why you would buy a car with just an accelerator pedal, and only forward gear, but most investors buy just that: no shorting, long only for ever. Must be nice to have a mind wedded to constantly rising prices (which long only implies).

PE is just that, so you are buying for management endlessly improving, but adding into the mix a belief in high gearing. You also believe that the managers will constantly be selling and buying investments at a profit. So, you must endlessly mark up your stock, to shift it too.

Can it really work like that?

Markets do not agree.

So, while there are many eye-wateringly deep discounts in PE, markets expect debt to blow a few things up and prices to sell stock to be cut back hard. With some reason, big banks have a shed-load of deal related debt stuck on their balance sheets, probably a fair bit of equity too, and no one is underwriting an IPO, if there is a scintilla of risk left involved. So, unless it is marked down, we have a stand-off, a buyers’ strike.

And in tech, the flaky stuff (AIM etc) is back down below pre-COVID levels, and possibly still falling, which is logical. The better stuff, but with an FX impact, bottomed out a while back, possibly in June? The big “portfolio” quoted holders did so in October, when discounts maxed out around 50% and the FX (i.e., dollar) tailwind was keeping asset values rising.

NASDAQ - a proxy for private equity

However, the NASDAQ hit a new low on 28th December, and that looks much less like a clear bottom, more a long base from October. It is a tough call; NASDAQ multiples drive PE valuations, so that is not helping. Investments with three year’s money a year ago, now have two year’s cash and judging by the speed of layoffs, know that when that drops to one year, funding lines either dry up, or get super pricey. And I don’t see FX helping much this year.

So yes, massive discounts, but also yes, huge lags and the normal discount implied for firms that mark their own homework on the valuation side. Audit firms may also be growing more supine (or getting sacked if they ask the real questions).

So, on a five-year view the sector is fine, even cheap, but on a five month or five-day view? The jury is still out.

While the PE sector is still looking better than REITS in terms of recent prices, it is still, in our view, the one that has yet to base out. If the reason for revival is a flourishing IPO market, that feels more like three years away; by contrast the stability in interest rates that REITs need will probably arrive this year.

So, we stay in touch with both areas, but by no means all in - not just yet anyway. But nor given the performance and yield they give, can they be ignored for ever.

Welcome to 2023.

Charles Gillams