The Scottish Play: Luck or judgement?

Three topics this week: has Sunak’s luck changed? Has India’s bull run ended, and where is this much-discussed recession?

The Art of the Possible

Image from Wikemedia - by Neide José Paixão

Looking at Absolute Return – Can it be Done?

A wise old hand once told me that all investors want is protection from inflation; do that, earn your fees and your job’s done. Read more

Reflections & Predictions

This year won’t be last year, that much we know. Nor indeed will it be the inverse, which is inconvenient. So, starting this year as last year, but simply turned face down on the desk, is a trap.Read more

All Clear? REITs and Private Equity

When do we go back to property (REITs) and private equity (PE)? We look closely at these two areas, as there appears to be nothing new to see or say on interest rates or inflation.

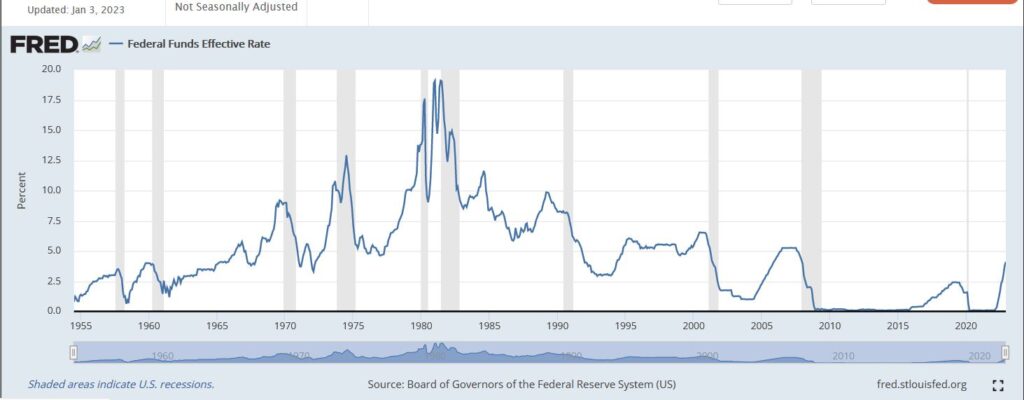

Macro is dull just now

Neither the Fed nor the Bank of England, nor indeed the ECB meet this month. So, the default is to assume a half point rise all round. Which should mean Western central banks are broadly aligned for a while, so by implication are currencies.

Clipped from this site – downloadable from source.

Recessions lag rate rises, so are not due yet either, although clearly one is coming.

Inflation will probably drift lower, but the employment markets stay strong, as the shuddering readjustment out of COVID continues to keep churn elevated. In person service hires roughly balance stay-at-home sector losses for now.

Basic food commodities, which have driven much of the recent inflation surge, will stay elevated until the current crops/stock are harvested and replanted late in the spring. Energy is possibly oversupplied for this winter. So not that much change in those two inflation drivers yet.

REITs

So, when is it safe to go back into risky assets? We look at two contrasting stories, firstly REITS which are seen as bond proxies, so cannot properly bounce until rates top out. This seems to need a couple of months at “no change” from the Central Banks. We are less sure about quantitative tightening ending, but most of the market gets spooked by that too. We think it matters little, because masses of global liquidity make what US banks hold somewhat irrelevant.

Nor do we see why REIT assets held on 7–8-year leases with typical debt fixed for half that term, should oscillate so violently over a few months, but that’s life, they just do.

Does property matter?

Institutional interest is not high, we know that, and most institutions need daily liquidity before all else, which lumpy property can’t give. Plus, for boring old REITS a lot has changed for the worse.

Who knows where retail space settles? It remains over supplied (and overtaxed), likewise probably office space, with the added wrinkle of retrofitting for carbon neutrality. COVID created an excess of new storage and warehousing, which also needs to be worked through, so that’s not safe either. While no institution wants the grief (or bad publicity) of dealing with individual tenants and homeowners, so we have long thought if you want to play the residential market, buy high street banks, as a kind of proxy. Mortgage lending is about all they do now.

It is private investors who still love property as a tangible asset; most are over invested in property and have been over rewarded for being so. Habit really. But if they had that habit before, they are still keen to know when to step back in, at bargain basement prices.

Private equity

Now PE, is a bit different. Yes, private investors like it (like hedge funds) but trust it about as much. Never sure why you would buy a car with just an accelerator pedal, and only forward gear, but most investors buy just that: no shorting, long only for ever. Must be nice to have a mind wedded to constantly rising prices (which long only implies).

PE is just that, so you are buying for management endlessly improving, but adding into the mix a belief in high gearing. You also believe that the managers will constantly be selling and buying investments at a profit. So, you must endlessly mark up your stock, to shift it too.

Can it really work like that?

Markets do not agree.

So, while there are many eye-wateringly deep discounts in PE, markets expect debt to blow a few things up and prices to sell stock to be cut back hard. With some reason, big banks have a shed-load of deal related debt stuck on their balance sheets, probably a fair bit of equity too, and no one is underwriting an IPO, if there is a scintilla of risk left involved. So, unless it is marked down, we have a stand-off, a buyers’ strike.

And in tech, the flaky stuff (AIM etc) is back down below pre-COVID levels, and possibly still falling, which is logical. The better stuff, but with an FX impact, bottomed out a while back, possibly in June? The big “portfolio” quoted holders did so in October, when discounts maxed out around 50% and the FX (i.e., dollar) tailwind was keeping asset values rising.

NASDAQ - a proxy for private equity

However, the NASDAQ hit a new low on 28th December, and that looks much less like a clear bottom, more a long base from October. It is a tough call; NASDAQ multiples drive PE valuations, so that is not helping. Investments with three year’s money a year ago, now have two year’s cash and judging by the speed of layoffs, know that when that drops to one year, funding lines either dry up, or get super pricey. And I don’t see FX helping much this year.

So yes, massive discounts, but also yes, huge lags and the normal discount implied for firms that mark their own homework on the valuation side. Audit firms may also be growing more supine (or getting sacked if they ask the real questions).

So, on a five-year view the sector is fine, even cheap, but on a five month or five-day view? The jury is still out.

While the PE sector is still looking better than REITS in terms of recent prices, it is still, in our view, the one that has yet to base out. If the reason for revival is a flourishing IPO market, that feels more like three years away; by contrast the stability in interest rates that REITs need will probably arrive this year.

So, we stay in touch with both areas, but by no means all in - not just yet anyway. But nor given the performance and yield they give, can they be ignored for ever.

Welcome to 2023.

Charles Gillams

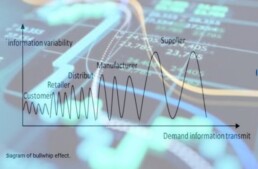

Bonds and Bullwhips

What are bonds for? Not always what you think. And the whiplash of the economy, (the bullwhip effect on all markets) makes recession both inevitable and meaningless.

Corporate bonds vs government bonds

So, to compare bonds - a corporate bond is issued to fund a project to produce a return greater than the interest and principal, and then pay the lender back. Much of the value lies in the assessment of how reliable that redemption is. Some of it is also whether the bond is cheaper or more expensive than a similar one, some of it is who is allowed to hold that bond.

But value lies in redemption, especially at the shorter end.

So, on that basis, what are government bonds? Well, they are there to achieve other objectives, seldom involving either redemption or a cash positive lifetime. It is largely accepted that they are a funding device to load debt upon future taxpayers, who luckily can’t vote. And the price of the bond is just what investors will pay for it.

Market rigging

Governments will therefore try to directly rig the market, to avoid paying too much interest, by for instance, mandating all investors and especially pension funds should hold gilts, their debts, on the gloriously fake grounds that they are “safe”. Well, just remember this year’s disastrous collapse, down by a quarter at the long end, with plenty of volatility too, ‘safe’ they are not. But the regulators and professional bodies still peddle versions of the old homily about the percentage of bonds in a portfolio should equal your age.

They can also apparently use the rate of bond interest to control inflation (so they say), so raising it (and devaluing bonds) if inflation rises, albeit the causes of inflation have little to do with the bonds (or bond investors). Then most marvellous of all, they can rig the price by easing and tightening their ‘quantitatives’ at will. Although no one is quite sure what a quantitative is, or indeed where it lives.

So, the government bond market turns out to be pretty much whatever you want it to be. To be contrasted with the weird and feckless equity, whose value can be, pretty much whatever you want it to be. Or indeed bitcoin, whose value….

A difference of degree granted, but less clearly one of substance. Rigged markets in any asset, make us nervous, and all markets are increasingly manipulated, to some degree.

What of bullwhips and earthquakes?

Well, both show a declining sinusoidal wave, that ripples prettily along and disappears. Whether it is the globe scratching its toe itch in Tierra del Fuego, or an irritated ear in Reykjavik, it is very jumpy. Where you stand now can be higher or lower than yesterday; it is erratic, chock full of faults, and crucially, not smooth and cyclical.

So, measuring whether you are higher or lower than last week’s datum matters little, if your fields have vanished into the sea, or indeed your sea has become a field.

So it is with recessions, after the shock we have had, being up or down two quarters in a row is trivial. Indeed, as that slick whipping wave races by, we will certainly be both.

Do changes in the Government bond markets matter?

And trying to decide whether the gyrations in the government bond market have any relevance to the level of the economy when the whole structure is bucking around, is slightly crazy. Nor are yesterday’s maps going to be of any use.

That is even assuming that the price of bonds has any relationship to anything except how little governments want to pay for their exorbitant debts. While I have not even mentioned the wealthy autocracies involved in the same game.

And that’s the market muddle we are in. The US Central Bank is playing old style economics, using the interest rate to control inflation - hang the cost of debt, that’s a problem for Congress.

But the UK and European Central Banks are playing new style, because they fear that the usual medicine will be disastrous for their rather sickly patients.

And US stock markets are using that funny old, discredited, yield curve to predict a recession that is by their definition (two down quarters in a row) inevitable, but ignoring the COVID earthquake which has upended all our old data and assumptions, simply because we have never had one like that before. The curse of econometrics is that we can only predict the future if it resembles the past.

EU stock markets

Meanwhile European stock markets have understood rates are not going up much more, because the EU would prefer to rig the market, so investors think they must have avoided a recession, which is equally a delusion.

And underneath all that is the great big chunk of molten sludge at the core, the vast irredeemable mass of government debt, where real yields are apparently staying submerged everywhere.

So wise men can select from all of that to predict that markets in debt and equity are going to go up a lot or down a lot, really as you wish. And they may all be right, at least somewhere on the globe.

Our own choices

But we still see no point in holding state debt, nor much in holding cash for too long. Corporate debt and equities, especially equities with a real value that you can figure out, maybe. We look at ones without state interference rigging the price, and with an ability to raise prices to hold margins, and which have a dividend yield. Those, we think, may still be attractive.

And we are not alone, many markets and stock prices bottomed out in October and are steadily inching up. Our own MonograM momentum models (both in the USD and GBP versions, a rarity this year) have triggered a re-entry into equites, and for once in a while, not US ones.

Something is shifting under our feet. So next year at least, is very unlikely to be like this year.

When we next write the calendar will have changed and no doubt many rate rises will have happened. But we doubt if the big themes will change much.

In the meantime, Seasons Greetings and a prosperous New Year, to all our readers.