Wood for the trees

We have all been obsessed with rates and inflation, but we seem to be in danger of missing what looks like a widespread bull market running broadly from last October. This is widely applicable outside the main US markets, including in gold. There is a similar and at times masking trend of dollar weakness.

What are the implications of this?

We also look at the unending tragedy of the various remnants of the Tory party.

Still Rising?

With markets still fixated on the next crash, we can sometimes overlook the long momentum swings. Although the US banking crisis matters, it is of little relevance to the far more concentrated and tightly controlled Basel III banks in Europe. Many would say to excess, but they are clearly tighter rules. The few assets not marked to market are a footnote in Europe; in the Wild West of US regionals, they can be the whole story.

On a one-year basis, the France CAC 40 is up 14%, the German DAX by 12%, with both the UK large cap and Japan’s Nikkei also positive, so equity markets have been strong, almost regardless of rate rises. The US is the main home of negative twelve month returns, but the gap between the S&P and the NASDAQ declines over that period, is now quite small, after the spring bounce back in the latter.

What does that mean?

For all the media love of the disaffected trashing their own communes, doing the right thing on pensions (they were very out of step) apparently helps France.

While the splitting of power in the US Congress and the meanderings of a senile President, has perhaps hurt the US, with everything from banking regulation to the debt ceiling made into a political game.

Brazil is down too, but India and Russia are up.

Well perhaps I go too far, but maybe there is a pattern? Markets like stability.

Relative values

While comparisons are complex where accounting systems diverge, the UK still looks like the lowest rated with the highest yield, and conversely the NASDAQ still has (by some way) the highest rating and lowest yield. US earnings are it seems still much more valuable.

The savagely anti-business stance of the UK, including a brutal rise in corporation tax maybe part of it, it will create a fall in earnings (and likely dividends) next year.

While the less visible, but still onerous onslaught in the US, including a minimum tax take, won’t be good.

So, does inflation matter?

The UK perhaps is also seen as the one major European market that looks to have dithered too long on controlling inflation (which could explain sterling strength). However, I see no real appetite for more austerity in the UK, so I find that assumption slightly puzzling. Having the FX market convinced UK rates are going a lot higher (because of policy failures) is hardly comfortable, but feels a little like re-living last year now.

Oddly too, controlling inflation the US way, has hurt equity markets more, it seems, than letting it burn out in the European style. Heresy to many of us, but that’s what the numbers imply.

All the theory, all the historic data says we now must get a sharp recession, but then grandpa, pray where is your beloved recession? Still looking, since mid February. It seems we must appease the inverted yield curve and believe base rates matter, but a bit more evidence would certainly help.

And rate cuts will be a powerful tonic, when they come. The bears are now reliant on widespread recessions, and soon.

Perhaps the best of this little bull market has gone, but there is a lot of liquidity still about and being out of the market with high inflation, is not great.

A multitude of sins – local elections coming up

And what of the UK Tory “Party”, if such a mess can be called that. The assumption for a while has been that the imminent local elections will be bad for them. However, they are a curious mix of voting locations this time, not London, not all of the Home Counties, none of the Celtic fringe, but a good chunk (but again not all) of the Red Wall seats. See map below.

Map from Wikipedia page on 2023 local elections

But really it is heavily biased to the Tory heartland, vast swathes of Labour free wards, where they are not even bothering with candidates, so it will not tell us that much. The Lib Dems will do well, but significant conquests in many areas will now require quite substantial swings.

The assumption is also that Dominic Raab was cut down by Sunak, who has yet to learn that throwing competent colleagues under the bus may feel good, but it thins the ranks of effective ministers, and builds up the malcontents. He has handled these badly, and forgets the real target is not his ministers, but his own position.

Tory strategy

Seemingly the Tory party has run just one electoral strategy for years, based on old victories; just trash the opponent. In a two-party state, voters must then decide who they dislike least. And both Labour (and the SNP) have reliably offered something so vile, that a simple victory follows.

But no longer, Labour (despite their recent rather crude posters) still seem innocuous.

The Lib Dems are sticking to their amateur politics, which can also look strangely alluring, if the other two parties look mysterious or inept. The Tories (like the SNP) are now in danger of being judged by results, not by fear or hatred of the alternative.

The score card on that basis looks pretty bad, and Sunak’s pledges are so far, going the wrong way.

Lend me your fears

I come not to praise Kwasi, but to bury him. This is an explainable, predictable but probably futile coup in the UK Tory Party, along with more King Canute from Bailey of the Bank.

But in markets there is abundant good value, but with few clues on how, or at what cost, inflation is to be tamed. Or indeed what may escape this time.

Political Manoeuvres

We have long noticed the Tory party’s splits and factions, broadly between the left and the right wing. This was a chasm Boris was uniquely able to bridge, by talking right, and acting left. The puzzle, as we noted, was why the left would bring him down to replace him with a right talking right acting Prime Minister. The preference was for a Blairite Conservative, low tax, high spending, but a steady reformer, with a lethal penchant for foreign wars and illogical hatred of the Euro. After Kwarteng’s departure, the Tories now have the doomed high tax big state faction back in charge again.

Hence the need for a pretext to overrule the party members and threaten Truss with the ever-gleaming sword of Damocles, held by the 1922 committee - we are back where the plotters wanted to be after Cameron – with the neutral Hunt playing the safe stooge to hold the fort.

Unlikely to win the next election

It foretells the inevitable party split – but we had never seen another Tory term as possible, regardless of the leader. Nor have we ever seen Keir Starmer as needing to do anything but sit tight and keep a grip on his party. If he is also spared the crippling cost of a really tight General Election, he can now face down the Trade Union money men as well.

As for Kwasi, if he stays the course, his troops will yet triumph at Philippi, he is by far the best the Tories have just now and looks to be the future. He has understood that if you fail to free the supply side, in a new productivity revolution, the current national decay will just go on, as it has for twenty years or more. But he has also not torched his future, Miliband style, in the wrong leadership move.

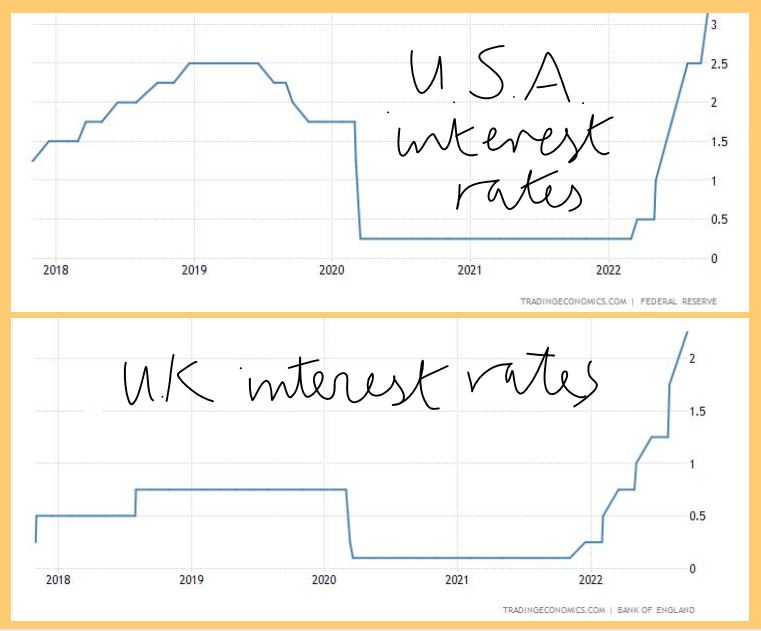

Will any of this stem the attacks by market traders? I doubt it. Will any of this forestall the inevitable sharp rise in interest rates, I doubt it. Or indeed stop ongoing sterling losses. To quell inflation requires interest rates above inflation, you can’t bear down from below. It remains daft to think UK interest rates can be effective whilst remaining underneath US ones either, as we said in our previous post.

Both clipped from this site, and set out side by side. The core data as is cited below are from the Federal Reserve and the Bank of England respectively.

So, what is the shape of this next recession?

I think we are now starting to see it. Not that much unemployment, the current tight labour market, without addressing increased workforce participation, is going nowhere. Nor is a secondary residential property crash certain. That is so last century, both areas are now far more heavily fortified sectors than they were last time. And both are now designed (and legislated) to be fiercely inflexible downwards. That is what the current labour market (and our dire productivity performance) is telling us.

House prices are propped up by a very generous market backdrop, ongoing vice like planning, high land taxation, tons of liquidity and a deep political fear of the consequences of a collapse. For all the moaning, borrowers are still able to load up at negative real rates, with a highly competitive mortgage market and generous fixed term offers.

But do expect a general slaughter of small businesses (or rather the current collapse will go on despite the various support packages). Expect weak margins for UK based firms, ever more exposed to competition, from far more generous and protectionist states.

WTO rules really are in tatters now and routinely ignored by powerful countries like the US and Germany. Expect a resulting fall in quality both in goods and services, again a continuation of current trends, as globalisation retreats.

But remember too, that so far, we do have inflation, but not a recession. The current dislocation is caused by a resource switch towards savers, who at all levels have had slim returns for a while, and we will now instead punish borrowers, who have had an absurdly easy, subsidised, inflationary decade.

The big picture, overall

Meanwhile in the energy world, a resource transfer is taking place from energy users to energy producers, who have likewise had a thin time of it. That those energy producers are places like the US, Russia, Saudi Arabia, Iran, Nigeria, Brazil, is a remarkable own goal for Europe.

But it is neutral for the world.

Indeed, much of those surplus funds will now be collected as various direct and indirect tax revenues, or to pay down debt, or as new investable funds, or distributed as dividend payments, but very little of that vast energy price transfer leaves the known universe.

For Europe, however the decline happens with the slow loss of productivity, plus the demographic torque. Meanwhile borrowing our way out, is suddenly becoming far more painful.

The political turmoil is ultimately from this change, and the longer states borrow more and pretend nothing has changed, the less effective will be their remedies. And indeed, the more the big efficient producers, like China, the US and Saudi Arabia will thrive. Neither more debt, nor protectionism will solve this, nor indeed will more global military adventurism.

Confidence is understandably damaged

Given that backdrop the mood music is damaged just now. Markets are trying to spark rallies, but with no real confidence yet.

Investors sense there is value, but with too little data to know where.

But whisper it quietly, Santa Claus is due, and the market mood is not quite as bleak as events suggest it should be.

The Turn of the Screw

So, we have Truss now. The continuity candidate, not the dull man who would take away our sweeties. But also, the same old Fed, keen to do just that. And its time we took a look at Starmer, the other continuity candidate and an excellent book on him; required reading for serious investors.

Otherwise, it is always a good summer when nothing changes. Markets swoop and soar vainly trying to catch our attention, but the reality remains that rates have to rise enough to destroy the excess demand that causes inflation. And they have to rise to equal or surpass that level, eye-watering as that prospect is. It will not be over until the US jobs report goes negative, and stays negative; anything less is prolonging the pain.

Presentation over substance

But this is a time of intensely political Central Banks, headed up by people without a grounding in economics, but a lot of “presentation skills”. They will be dragged kicking and screaming and smiling to do what they should have done last year, hoping vainly for some supply side reform or windfall to help out. But largely still facing the exact opposite, populists who think subsidies “cure” or ameliorate inflation.

Markets are oddly buoyant; they get like this at times, but we see that as a mix of delusion, the self-reinforcing strength of the dollar (be very careful of that one, it is a new bubble) and the spluttering remnants of buying on the dip.

But be under no illusion, Central Banks trying to guess where the economy is going is like fly fishing with a jar of marmite. Entertaining, but highly unlikely to catch anything.

Truss: Issues and options

Truss meanwhile looks like a re-run of Boris; it won’t be quite that simple, but it looks like more style over substance, a different set of lobbyists, but nothing really changing. The idea either she or the EU can afford a bust up with the UK, just shows how silly markets can get.

Some of her programme may make sense, both the NI (tax) rises, and the corporation tax increases were badly timed and should be reversed, given inflation is doing the hard work already through fiscal drag (or frozen tax thresholds).

The rises were proposed when we were exiting the COVID crisis, but before we understood the energy one. We said so the last time we wrote to you.

Ditching a few Treasury backed white elephants (HS2, Freeports, the crazy fiddling fetish on capital allowances) would do no harm either, but overall, the market’s verdict is clear: fiscal responsibility is still a long way out. We can all see how sterling has collapsed against the dollar; it is less clear why it has fallen against the Indian Rupee or the Chinese Yuan.

Source: See this website for all the daily data.

A book to read for all investors

So to Starmer, the likely next UK prime minister, where we need to pay more attention. Both on his mindset and on why the Labour Party hates him so much. Which in turn explains why (and with the Tories fatal ideological split heading them into Opposition), he is so fixated on party control.

Oliver Eagleton writes very well. His recent book The Starmer Project looks at four episodes, his left wing legal start, his transformation into a Tory enforcer with a penchant for exporting judicial expertise to the colonies (don’t laugh), his alleged machinations to back the People’s Vote nonsense to bring Corbyn down (pretty dense stuff, even now) and his use as the Blairite stalking horse to put a stop to Corbyn’s chiliastic tendencies, (which also gives you a trigger warning about a light dusting of Marxist ideological claptrap).

So Starmer is all about what works, which would make a nice change.

We’re looking at a very global mindset, apparently quite a strong Atlanticist outlook, keen to work with European authorities, but aware that the Brexit boat has sailed. An interest in devolving power down, but keenly alert to the risk of anarchy that entails. Indecisive, a Labour Party outsider (on his first election in 2015, apparently his nomination had to be held back to ensure he had the minimum length of prior party membership). Starmer is not exactly collegiate, but he has run a Whitehall department (as Director of Public Prosecutions) so not a loose cannon.

Very London too, Southwark, Reigate, Guildhall School of Music (sic), Oxford for post grad law, Leeds as an undergraduate. So should at least know where the Red Wall was. But lest you relax too much, a total ignorance of economics or business, let alone how to create growth. It won’t be easy.

And what about Markets?

Well for a UK (or non US) investor you only had one question this year. If you ditched the local currency you made money, and if you held onto sterling you got hit. Our GBP MonograM model is doing fine, it got that one big call right: kind of all you need. If you are a dollar investor, outside of energy your best place was cash. And our USD model took longer to spot that shift. As for active investing, sadly pretty much the same, the dollar is the story, or dollar assets. All of which perhaps makes dollar earners in the UK look cheap still.

But for now we see the story as a currency one, and at heart that is just about the timing of tightening interest rate spreads. The widening of those spreads has caused the recent havoc.

So when (finally) the European and UK Central Banks abandon futile incrementalism and get the big stick out, that will call the turning point.

Charles Gillams

The Times They are A Changin’

Rishi or Truss, can either be worse than Boris?

Also, we do seem to be decisively leaving the decade of low rates and by implication the experiment of quantitative easing. On a twelve-month basis, bar the FTSE 100, all major markets are down, although that is only just true for Europe and Japan. The Nasdaq and Aim are the big losers, and their recent recovery looks like a head fake to us.

We look at the global economy, and investment options.

So, what does the race for the next UK prime minister now look like?

It is not that important anyway, if as I assume, the next election is lost already.

These are stand in candidates, with no real grip on the party and likely to be loathed by the surviving group of Tory MP after that 2025 contest. Like a relegated football manager, they will have shaky job prospects.

Is there much to choose between them? Again, I am not sure, they have established that the party to its core hates higher taxation, whatever fantasies Boris had, and some at least understand that a smaller government or higher debt, is what the hard choices of governing are about.

I rather expect much of the ‘difficult’ stuff attempted by the last Cabinet will get ditched by new ministers. It still would be wrong to say the new team can’t achieve much, the governing majority is solid, and further bloodletting inconceivable. I would anticipate that they will still have two and a half years to run.

The two candidates compared

Sunak is admired for his high-profile experience as Chancellor, disliked for his willingness to raise taxes, loathed for wielding the knife on Boris. Truss is thought to be opportunistic, and rather unfairly for being dim and not substantial.

But I don’t expect much of a change, more fiscal conservatism, less besotted greenery, perhaps less socially liberal, but only to the extent of holding the line, not really rowing back. Short term stability, long term decline.

Preparing for another European killing field?

But you do feel Sunak would be less of a cold war warrior.

The report that the Chief of the British General Staff had called this “our 1937 moment” and launched “Operation MOBILISE” suggests the bloodlust is well and truly up, all adding to the hefty training programme. We are already deep into a proxy war ourselves.

I hear it is just as insane in the Pentagon. There is even high level gossip about this being the final great “killing field” in our centuries’ old hostility to Russia.

Economy : two questions affecting interest rates and inflation

As for the global economy, we had two great questions for the year, how long could the Fed “extend and pretend” over inflation, and how quickly everyone else would then play catch up.

Well pretty well the day Powell was re-confirmed earlier this year, he binned the Jackson Hole pretence that high employment did not have to mean high inflation.

I suspect (and so do markets) that he won’t really go after inflation, if he did so, we would have interest rates in double figures by Christmas.

Bread, job, and a roof, these three a politician must provide, and just one without the others, is a vote destroyer.

The current modest level of rate rises will let inflation creep lower, but will not control it, and we don’t see interest rates topping out for quite a while, not helped by the very low starting point. Although overall, it looks like the currency markets are forcing the rest of the world to follow in raising rates quite fast and in the end, to the same levels. Nevertheless, in Europe the response to double digit inflation, has so far only extended to ending negative rates.

As if that will matter, as the Euro collapses; they will have to move faster. Lagarde confidently delivering total guff and mysterious lawyerly threats won’t save Italy.

The economic models everyone is relying on to forecast otherwise, seem to assume no incremental rise in energy prices next year, and indeed a sizable fall. That maybe so, but there will still be a lag as this year’s rises have not been fully absorbed and will echo and bounce around the economy for a while to come. Not least through a still very tight labour market, which has several years of lost capacity due to COVID and indeed the familiar demographic time bomb.

A slackening in wage inflation needs US and Northern European unemployment to at least double; no sign of that yet. It is a muddled employment market with spatial and skill deficits, so increasing capacity where it matters, will take time. Not least because of persistent high surplus labour levels to the South and West in Europe.

So, if the Fed (and Wall Street) insists (as it does) on calling this transitory inflation, or now the new phrase, ‘peak inflation’, they are simply using dud econometric models (again).

What next?

Cash flow will again be king, capital will be well rewarded in the bond markets, dividends will have competition, non-dividend payers face a long winter. Experience of the dot com bust, and then the banking crisis, suggests it takes three or four years to retool models based on prior poor capital allocation (and boy have we had that). Not the three or four months which is being assumed.

Granted we were oversold at 3666 on the S&P 500, perhaps an auspicious low. Yields meanwhile had shot out beyond reason, but reluctantly we consider this pleasant bounce can’t survive. We accept too that earnings are OK, but they are in most cases a poor indicator of economic forces that take years to establish themselves. The extinction of even capitalist dinosaurs takes time.

And then there is the great concertina of rates: ignore what each Central Bank says, in the end they must march to one beat, that of the dollar.

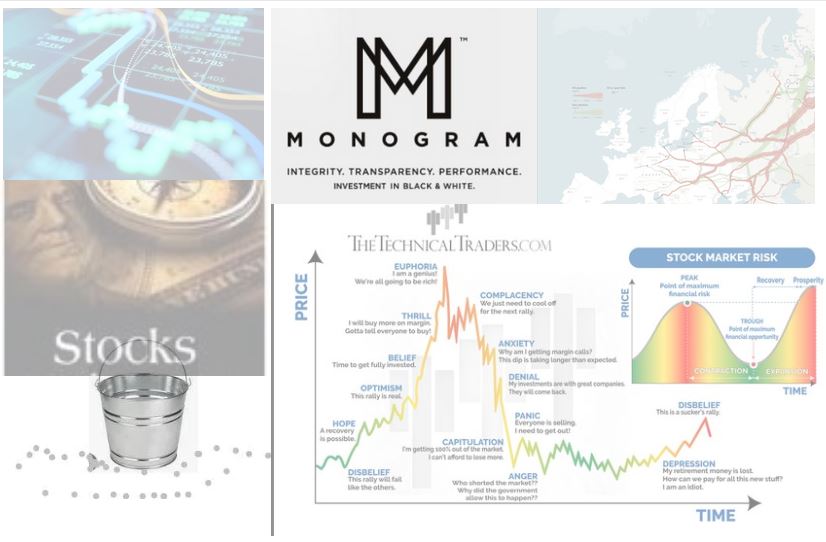

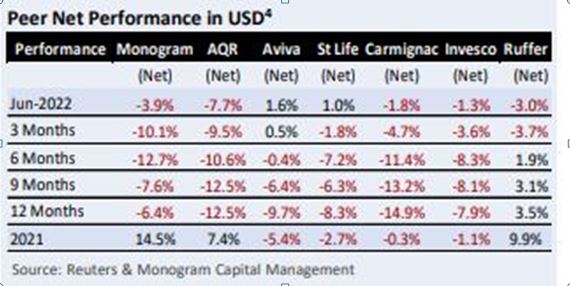

Monogram performance, compared to others in the Absolute Return sector

It is striking that our USD MonograM model now holds no equities or bonds, our GBP MonograM model is fully invested in both. While the list of storied Absolute Return managers who fail to beat our model remains embarrassing.

Download the newsletter of which this table is a section, for the full data.

There is no availability of this model, except through ourselves; perhaps it is time to talk to us about using it?

Do get in touch, an exploratory discussion is never wasted.

We wish you a pleasant summer: as good Europeans, we will fall silent for August.

I hope it all looks clearer when we return.

Charles A R Gillams

Boris finally quits, and 'Quality Growth'

Boris finally quits: the loss of his Chancellor clearly made this inevitable. We also reflect on the London Quality Growth Conference, held in Westminster last month. It implies a very US bias, driven by two US universities, that seem to dominate much of UK investing and indeed public policy.

First as tragedy, then as farce

So, it is over. The absurd repetition of the same error and the same apology passed from tragedy to farce.

Clearly the belief that you fight inflation and unpopularity, by bankrupting the country with printing money, had also simply become too much for Sunak. That was the fatal blow. Let us hope the next leader is less of a deranged populist. In the real world what is popular seldom overlaps with what is right.

We will skip the look backward, over his flawed career, skip the look forward over the seven dwarves, and fervently hope for a different set of economic policies by his successor. It sounds as if there is plenty of time for a long summer of speculation. The likely candidates are less than attractive, let us say.

How might the UK market respond?

Nor can I fathom a market response to a change of leader in London: bullish that it is over? Or could it be bearish as we don’t know what comes next, or indeed bearish in that it surely strengthens the opposition?

While we felt the Old Lady moved far earlier than others (late in 2021) because of UK fiscal laxity, we see no reason yet for them to back off their August rate hike. Politically it is hard to stop and start interest rate moves, while just repeating a previous measure in mid-summer will look innocuous. I suspect that’s true for September too, but that feels a long way off. And I do note, that as we predicted, the great spike in corn and wheat prices has taken just one growing season to unravel, as farmers react quickly, by adjusting cropping patterns, knocking out another justification for any more price rises.

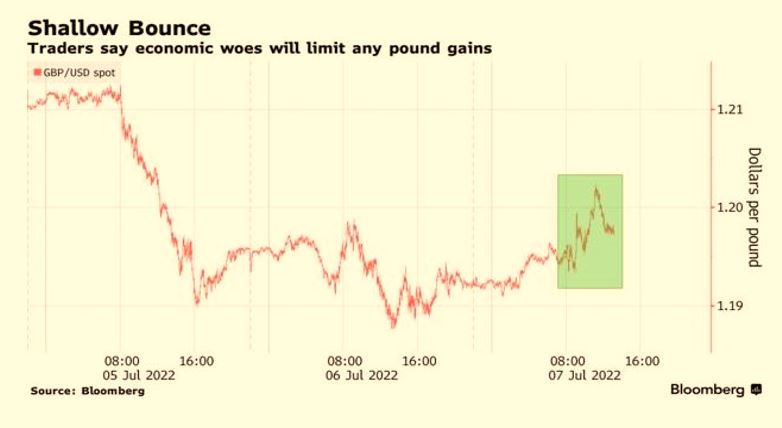

A weak pound is also importing inflation, and the Bank has to make a stand somewhere, but 1.19 to the dollar feels too early, 1.09? Pressure will start.

Alchemy Unchained?

We turn now to ‘Quality Growth’, an excellent conference and well presented with a dozen first rate managers from the US, UK, Europe presenting.

But it led me to ask about the underlying assumptions of the ‘Quality Growth’ model.

Firstly, there is the Santa Fe school, which speaks of the ultimate failure of nearly all quoted companies. This is the old ‘99% of the S&P 500 stocks contribute nothing to returns’ case. Allied to that is the Columbia (New York) mantra that some companies can beat the pack for ever, so the theory is find those “compounders” with their ‘deep moats’ and your investors will win for ever.

It was surprising how much of current fund management practice is wedded to those two assumptions. They look remarkably shaky to me, but if believed by enough of the industry, are likely to become self-fulfilling.

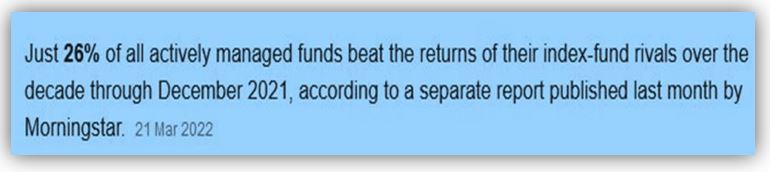

Which adds to another oddity: we know active managers seldom beat index investing. But this year should be showing the exact opposite. Passive long only funds are destroying wealth at a terrifying speed. So true active managers should do well too, but oddly (and absurdly) perhaps because of this “a few chosen winners” theory, they too seem to willingly forget about valuation.

True Believers

You see these few companies are (after exhaustive analysis) the nailed-on winners, so if the market halves, they will still outperform - just hold on and they will come good, the fundamental long-term analysis says so. You will recognise Cathie Wood, Scottish Mortgage are, in some measure, exponents of this too.

What is not to like? Well, self-reinforcing buying propelling valuation is dangerous; ask the Woodward investors about that one. But we also get odd clusters (identified as the winners, or the winning group, or amongst which will be winners; choose your terminology, like Tesla or Palantir or Netflix), which cut loose from sane valuations, becoming for a while mere intellectual Ponzi schemes, moving only upward, fed by endless new money.

Until they don’t.

And every time ‘buying the dip’ gets burnt, there is less fuel for the next attempt, and less appetite to try.

Too narrow a view?

I am not wholly convinced by the ‘only a few stocks matter’ theory; for a start, you have to be very lucky with your baseline, even if you can spot the gems.

But even less do I believe that you can really thread the needle to identify the great companies, and secretly buy them, without shifting their prices and then hold them, in public portfolios. If you are right (and success requires you to be right) then everyone else piles in, and valuations simply become a function of overall liquidity.

The belief that having found them, you can leave them in your portfolio for decades, feels somewhat quaint. There are some giants that do perform year on year, but we all know of plenty of giants that rise and stumble (see above), and many that have multi-year slumbers (most oil and bank stocks).

Fashion or Momentum?

So, at the conference, we had a hall of great fund managers, but also the odd IFA pleading to be told about current performance, which was simply shrugged off. Our clients are always keen to be told about our recent performance, I am sure in truth so are theirs.

Given the structure of the market, now may be the perfect time to buy Quality Growth, but that bigger question about rates and inflation trumps all. And investing, we know, is about fashion, that’s why momentum (usually) works.

I do like some of these funds, and respect their hard-working managers, but feel investing needs a hybrid approach, quality, yes, growth yes, but critically valuation and momentum too.

It seems like public policy has also increasingly drifted in the direction of this “picking winners” theory and backing what are believed to be high yield, clean, desirable industries, rather irrespective of their viability.

Public Policy implications

Once you accept fund managers can spot these, you perhaps accept governments can also nurture them and scatter tax breaks around them. This will, at the same time, destroy the rest of the commercial ecosystem, in part, oddly to fund the hoped for predictable and desirable elite. Look at what Tesla (again) has done, extensively subsidised by exchequers round the world.

Does real life work like that? I doubt it - but investing theory has clearly now tainted public policy too.

Charles Gillams

Monogram Capital Management Ltd