Investment, Politics and Economic cycles

An intriguing current question is which cycle are we in now? Is it the 2000 to 2022 one, or the 2008 to 2022 version? We look at the arguments, and the politics behind it all. And who exactly are energy sanctions designed to hurt?

Hopefully, everyone has now understood it is not the 2020 + rate cycle. Why should it matter? Well, the implications for interest rates are startling. And indeed, for buying on the dip.

Interest rate cycles

If you consider that interest rates should be about 2% above inflation, to induce savers to defer their consumption, then this cycle really extends from 2000 onwards. The excess credit of that era, led firstly to the GFC in 2008. This in turn led to sudden a lack of credit, but ultimately exactly the same problem of excess debt has reappeared in 2022. The efforts to dampen cycles, seem to just exaggerate them. As does using the same remedy for two very different problems.

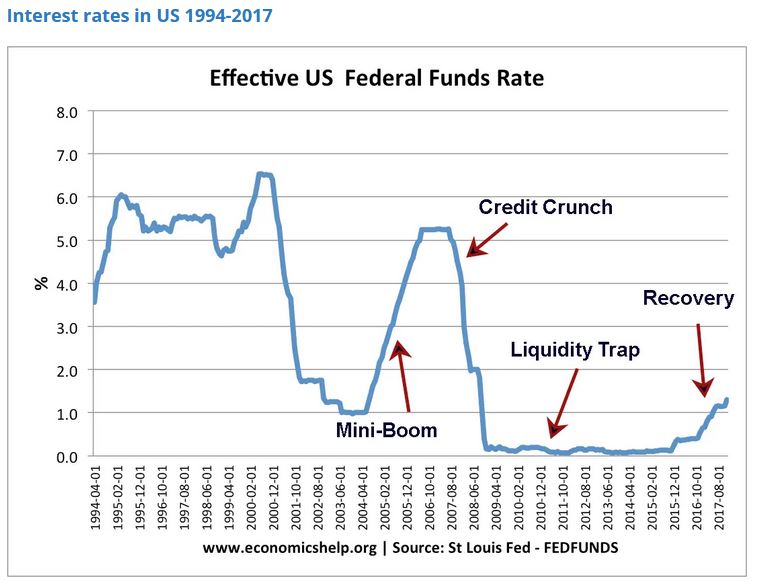

Here’s the US picture from the late 1990’s to 2017

In a similar way UK Base Rates in January 2000 were 5.5%, as they were in December 2007, before a long descent to 0.25% in August 2016 which largely held (with a few bumps) all the way to December 2021, when they were still 0.25%! That was before the recent rather modest rises. So, by our “inflation plus 2%” measure of sanity, October 2008 was the last time base rates were sensible.

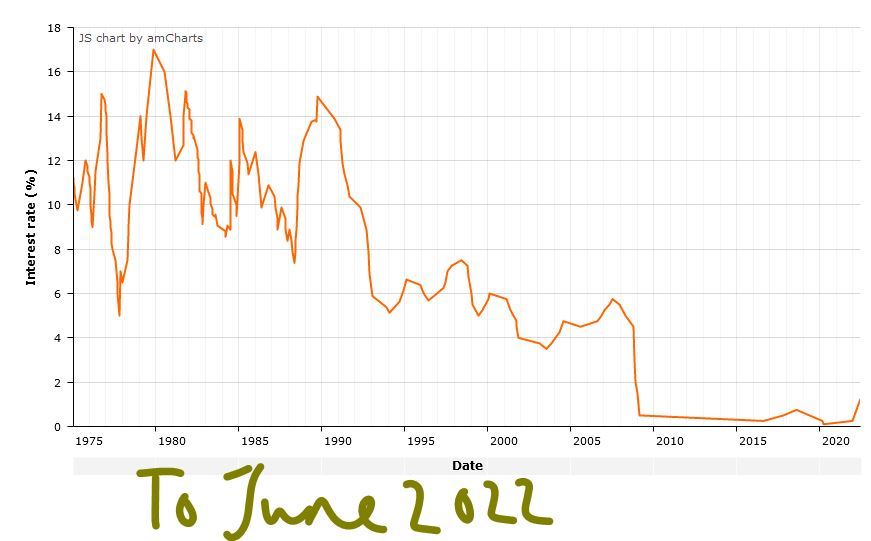

Ref: this stats article

In other words, this crisis was foretold. SPACs were an early indicator which we mentioned back in 2020. So, if the GFC was caused by too much credit in the US sub-prime housing market, will the hallmark of this one be excess speculation in meme stocks and crypto currency? Clearly, we have now learnt that these “assets” are all distinctly well correlated with each other.

In which case, banking regulation was only half the answer to these vicious moves, because the regulatory perimeter is always too tight. The vandals will inevitably camp just outside the walls - wherever they are built.

Will inflation auto-correct?

It also raises the question of whether the “cure” to moderate this economic cycle is going to be a continuation of the same lax monetary policy. A rather fuzzy consensus has formed around the 3.5% level for interest rates to top out, falling back down in time.

We accept that is roughly the market belief, but feel it needs big assumptions about the auto-correction of inflation, which is presently just a fervent hope. In the real world (as distinct from asset bubbles) interest rates are too still low to matter, and we still have negative real rates on an exceptional scale. If Central Banks are really hoping to correct the laxity of 2007 to 2022, they will not stop at the current levels, but will go far beyond and cause a proper recession. But if they just want to re-establish the post 2008 consensus, they will go easy. They are talking about the former, acting like the latter with all their foot dragging and funny fixes. Is Euro fragmentation sorted? We doubt it. But if it is, they are not telling us, or really even defining what it is.

The ECB and our energy pricing policies

That partly is why markets are jittery, and why the ECB seeming to move from the cheap money forever camp (leaving Japan all alone there) to the appearance of being serious about inflation was so traumatic. We still don’t think they will tame inflation with interest rates alone, as by definition to do so breaks the Euro. This is because Italian debt in particular can’t be funded at any credible real interest rate. So, they too are just hoping for the best.

We also remain baffled by the West’s energy pricing policy that has created this sudden existential crisis. It was interesting to hear Boris telling a startled world, from Kigali, that not everyone feels creating a global food crisis is a rational approach to the Ukraine invasion. As if that was news, although it clearly was to him.

The politics behind it all

But there too we sense two underlying agendas.

Just as it is possible these interest rate rises are really to mop up the GFC policy errors, so also, a large part of the left is desperate for high energy prices. This includes the more thoughtful contingent hoping demand destruction will help sustainability goals (we ourselves have long advocated £2 per litre petrol, but gradually building to that over the last decade, not overnight), but also the more zealous, who are keen to exploit the crisis to render renewables competitive, that much sooner.

There are some big distortions in energy prices too, much of it created by the modern obsession with competition at all costs.

If this is so, then Russia is just a convenient excuse to ramp up carbon prices, blaming Putin for the resulting misery and achieving long-term goals. Certainly, Biden is acting that way, albeit, as ever talking the opposite way. Or rather his clever minders are.

There is a hint too that Boris is in the same deranged camp.

Oddly the EU led by Germany and Austria, with talk of restarting coal plants seem a little more pragmatic. Meanwhile the great beneficiary is Russia and the ever-stronger Rouble. They too have used the crisis to consolidate long term aims, not just in the war-torn rubble of Ukraine.

In short you either have inflation, or a credible short term means to create energy to replace Russian supplies, or high interest rates.

It is odd to think you would want to select just the first and last of that trio….unless your motivation was to correct another perceived policy error.

He who pays the piper

A very strange quarter: the FTSE100 was up, in sterling terms the S&P 500 was up, and the Russian Rouble ended where it was just before the Russian invasion. Short term dollar interest rates are nicely positive at last.

So where is the problem?

UK policy changes – could we finally be leading in economic policy?

Well, at long last the UK Chancellor has finally realised that just throwing money at inflation has one clear outcome: more inflation. This is tough lesson learnt back in the 1970’s and seemingly since forgotten.

If true it is a turning point and we predicted that it must always come sooner for the UK, if it persists in staying out of the Euro, than for bulkier continental currencies. Sunak also seems miraculously to be finally tackling some long overdue, multi-parliament, structural taxation issues, a rare sign of political maturity.

Whether he can hold the line against an increasingly dimwitted set of MPs and a media who constantly bay for more fuel to be added to the inflationary fire is unclear, but at least he has had the courage to step out into the unknown night, not cower by his warming bonfire of magic myths.

Nor is it clear whether he has the clout to unpick the cosy mess created by Theresa May and her childlike energy price fixing, or the ensuing nonsense from Ofgen. This fine-tuned capacity to the point of absurdity, guaranteeing a massive breakdown in the generating buffers, which had been painstakingly installed under a series of Labour governments.

Inflation policy is being taken seriously

But Rishi is trying; to cool inflation you simply must have demand destruction, there is no choice. This type of deep-seated widespread inflation will be hard to quell in any other way. True, areas of it can be contained, but it is hard to hold it all.

He is lucky to be helped by a Bank of England that seems to be serious about its brief, not regard it like Lagarde and Powell, as some kind of political inconvenience, to be wished away in double talk and evasion.

But he’s unlucky in other ways; we noted a while back that China no longer seemed to care about headlong export led growth, or more broadly about access to hard currency. It feels it can invest with and gain from its own currency and avoid importing the monetary excesses of the West. That in turn means it cares less about the endless flows of cheap goods to Europe and the US, and conversely about soaking up those surpluses in luxury goods and services. None of this is good for our inflation.

Meanwhile by eliminating the oddly divergent starting points for the two income taxes, National Insurance and Income Tax, Sunak has opened the way to many benefits. It continues to drop taxpayers out of the system, despite desperate measures by HMRC to suck more in. A key step, and a sign of, for once, a more liberal, more efficient government. Many more steps are needed to unshackle wealth creation, but it is a start. It makes much of the Universal Credit complexity around thresholds also fall away. Most of all it is a step closer to combining the two income taxes.

Politically this is highly desirable, as it strips away the pretence of a low starting rate of taxes on income.

It perhaps even gives an excuse for the otherwise inexplicable step of introducing National Insurance on employees passed retirement age. Given so much of current inflation is due to the mass withdrawal of older workers, another step in that direction looks remarkably stupid, but perhaps it has a higher purpose. It is good to see that the “Amazon” tax as Business Rates should be called, as it gives Amazon such a massive earnings boost, is also clearly still under long term review.

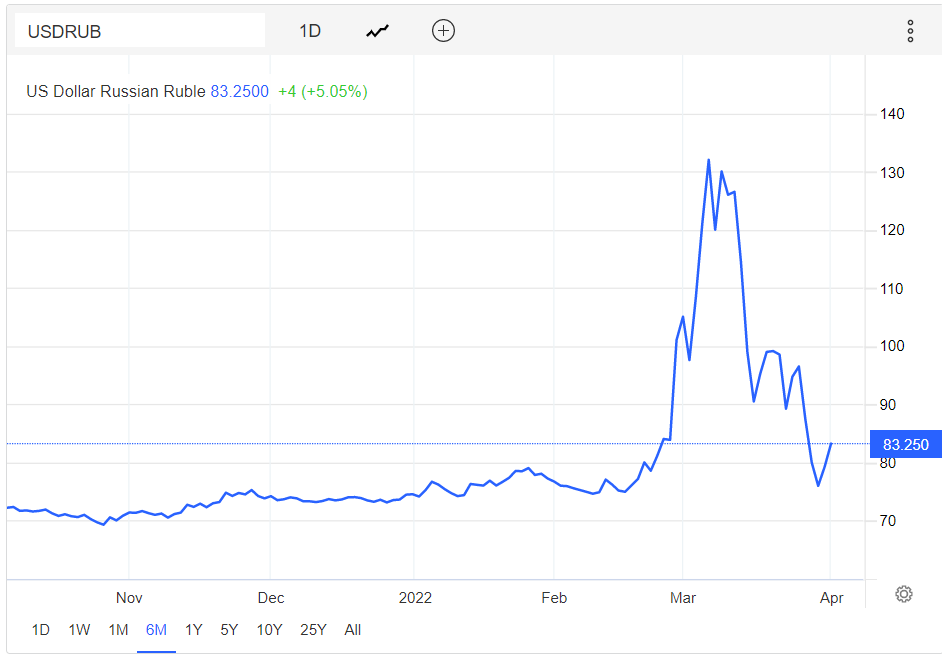

Why has the rouble recovered?

Source : this page on tradingeconomics.

The recovery of the rouble is of course not a market step alone, doubling interest rates, exchange controls and the mass withdrawal of exports to Russia from the West, are part of the story too. But it also shows a turning point. At first the West was so shaken by Russian military attacks, it was prepared to follow its own scorched earth policy, regardless of the harm caused to our own people and employers.

But at some point, the realisation that Ukraine’s army would hold, that Putin’s army was not that good after all, especially up against modern weapons and we start to understand that the further blowing up of our own bridges just raised the ultimate bill. Here are the sanctions we've imposed.

So, it seems it is no longer true that any price is worth paying to help Ukraine or hinder Russia. Clearly, we don’t have to jettison all our principles in dealing with other tyrants, nor one hopes do we need to alienate every piece of remaining goodwill with the rest of the world, by panicked grandstanding.

The mob is still rampant, goaded by an American president for whom no European economic sacrifice is too great.

But maybe it is also time to tell Ukraine that no NATO also means no imminent EU: Brussels has its hands full with its own struggling ex-Soviet states.

And what about Powell and his policy?

Well, we don’t expect him to hold inflation down with his trivial rate rises, nor politically can he do more than tinker. It seems too that Lagarde at the very least has to get Macron back in, before telling the bitter truth about rates.

So, we feel the bond market has rates where the market would like them to be, in the US, not where they will be set by the Fed anytime soon. And the Euro is now in a very odd place, still with monetary stimulus being applied and with an unstable gap to US interest rates.

So, we may look to be where we were late last year, but in most cases the cracks are now alarmingly wide.

Europe, quite urgently, but the US as well needs a sharp jolt upwards in rates to halt inflation.

Oddly only the UK looks to have spotted the danger, stopped the false COVID ‘economic expansion’, tightened fiscal policy, reformed taxes and raised base rates steadily, towards where they need to be. How unusual.

Long may PartyGate continue if this is the end result.

We will take a break for Easter now, and resume on the 23rd.

If the first quarter is a guide, by then everything will have changed again.

First Principles

Principles may be lacking in certain quarters, but we will start with the economics of inflation rather than Boris.

How much inflation and for how long?

Inflation is simply too much demand for the available supply, nothing more complex than that. So, you tame it by either less demand or more supply. So, unlike it seems most Central Bank economists, who it turns out are just statisticians, for ever looking back, we must project forward.

That tells us quite clearly that the inflationary imbalance will persist as long as demand stays artificially high and supply is artificially constrained. It is that simple. Forget the rest.

So as long as governments have fiscal laxity, along with negative real interest rates, they are pushing up demand. As long as workers won’t or can’t work, it will reduce supply, as long as economic activity is made less efficient by government action and diktat, it will reduce supply; end of.

So, at the very least Central Bank balance sheets must start reducing, which is not happening, stimulus must be fully withdrawn, which is not happening, and the old workers and their old ways of working must resume, which is not happening. Fresh capital can certainly change some of that, but it takes time.

Putin, Oil, and Geopolitics

What about oil?

This is the one item that alone might distort the picture. Which is positive, as we see oil prices falling in the summer. We also don’t see the West has really grasped what Putin is up to; in all the cold war style hysteria, he is possibly just after what he says. This is for the West to stop fomenting rebellion in Russia’s sphere of influence, and to be clear about NATO expansion plans, where there are indeed none in existence. He might have higher hopes, perhaps of a deal on Crimea in exchange for the Donbas, but we doubt it (or his chances of getting it are low). As might we, less interference in our politics would be nice; but see previous answer.

Nor is it that clear he is actually rationing energy; it is telling that Russia is reported as not able to meet its OPEC + quota, which at these prices is crazy. His oil industry will have been hit by sanctions, and the loss of Western expertise, and the Russian economy will also have suffered under COVID. A loosening of sanctions would really help him, for all his bravado.

If that reading is correct, as the situation winds down and OPEC+ winds up production, oil prices will fall, I would expect quite substantially. Much of the energy spike is self-inflicted, with nuclear plant closing or offline in France and Germany, and reckless price controls, having made using UK gas storage unattractive. All of these things can be sorted out.

Any possible good outcomes on inflation?

So, to inflation, well it won’t care much about the pinpricks inflicted by the likely interest rate rises now under discussion, especially if they creep up so slowly no one notices. It needs a unified 1% OECD jump to cool this lot down, and the ending of stimulus. Neither is likely. Closing the US printing presses, were it to happen, does also have interesting global impacts, as Andrew Hunt notes.

We see it all turning rather glacially, with a bigger slump in inflation, if energy prices fall, but then being generally persistent in the 3% area for the rest of the year. We expect to have both higher rates and inflation for a while.

All of this is mighty tricky for investors, but I don’t sense that just bailing out is right, nor that the actual interest rate rise will cause an enduring slump in all asset prices. Investors have to own something, or they will sit and be mauled by inflation.

And what of Johnson?

It is easy to read the current level of confusion from either side’s viewpoint. Yet to me, I see the normal factional infighting, the usual media exaggeration, some political mischief making, but still no reason to depose a Prime Minister with a very clear mandate and a large majority. Like any large party the Tories have the embittered and passed over, the Remainers and fans of state intervention and a volatile and raw body of new recruits in seats no one ever expected to win. Plus, no doubt a few opportunists who sense that the heavy lifting on COVID and BREXIT is done, and they can now seize all the prizes.

The Tories do need a reset; it would be nice if Downing Street left Ministers to govern and simply acted as a cheerleader. Not that I see that happening, leaders and their hangers on always lust after more and more centralization, more control. But until a compelling, unifying, plausible Tory opponent appears, I foresee no change.

And in a way with reform all but dead, with Gove’s last hurrah on ‘Levelling Up’ a damp squib, it may not matter who leads the Tories, they have very little real power.

It is quite odd how big majorities do so little good, and how poor party discipline is, when they have them.

Charles Gillams

THERE IS NO SANITY CLAUSE

Three big topics this week from three central banks, all of whom look to be in a muddle, with their knitting all jumbled up and highly implausible. Entirely predictable inflation meanwhile threatens to sweep them off their path, as they tinker with micro adjustments to interest rates.

Boris is diverting, but we doubt if it all matters; pre-Christmas entertainment. If he were logical or even vaguely numerate, he would change, but he’s not, and he won’t, but nor does he need to.

The Lib Dems win a by-election, that Labour fails to contest, but it makes no difference in Parliament, and it lets Boris look contrite mid-term. He will survive this with ease.

Which is not to say he should, or that he’s not making a hash of COVID, the sequel. In keeping the NHS in its current format, Boris fails to ask, as many have before him, whether it is still fit for purpose. This remains an urgent question. It can’t simply collapse every year.

Bailey - Bank Governor and historian

But perhaps Andrew Bailey, Governor of the Bank of England, understands the extraordinary risks Boris poses to the economy, and has hiked rates to show that. A Cambridge (Queens) historian, with a doctorate on the impact of the Napoleonic Wars on the cotton industry of Lancashire, he will know full well the impact of a French orchestrated trade war backed up by a dodgy pan European monetary system.

A consummate insider, via the LSE, he moved on to the ascending ladder of the Bank, which did include a slightly unfortunate move into the FCA. This turned out to have rather more real villains than he was used to. Married to the head of the Department of Government at the LSE, he will be very well aware of the political game and the current mood in Whitehall.

He’s seen enough inflation and has decided the Bank must pretend to act. Not only is the rate rise trivial, but it also coincides with a continuation of Government bond buying (QE), an odd call. That the last thing the economy needed was still more liquidity, has surely been obvious for eighteen months now.

Christine Lagarde and Jerome Powell

In Europe the same mishmash exists. We have been hearing Christine Lagarde explain why the ECB is now accelerating one asset buy back (APP) while ending another one (PEPP). She was winging it with the phrase “utterly clear” in answer to a pertinent question, when it was clearly anything but. Still, she did seem to have her ear rather closer to the ground on wage inflation, at least compared to Jerome Powell.

He by contrast has been caught with his pants on fire, trying to weasel his way out of the Fed failing to spot inflation, by saying that most market commentators agreed. Remind me, which is the canine, and which the wagging appendage?

Basic economics - why inflation arises

We called it on inflation as soon as that stock market rally took off, and for the simplest of economic reasons: the pandemic had reduced global productive capacity, so absent a change in price levels, the economy was less productive, profits were therefore lower, competition would therefore be less (unless prices rose), and total production must fall. Less output, same demand will always mean inflation.

Forget the energy issue, forget supply chains, less capacity, more demand always means trouble. True based on that one schoolboy error, the dopey measures to reduce capacity further by more regulation, hiking the minimum wage, paying people not to work and so on, plus embarking on accelerated decarbonization and a few new trade wars, was not going to help much either. But please no more “surprise” inflation, it was baked in. (See extract from my book, Smoke on the Water, blog dated July 2020, title re-appearing shortly on Amazon)

After the interest rate rise

However, we have also long felt that interest rates can’t rise enough to stop inflation, but that as governments have to back off fiscal stimulus, as they are already overborrowed, the lower productive capacity will itself shrink demand, and in the end cause inflation to fall. But we see that as taking years, not months.

Why are interest rates not rising to combat inflation? No political will for a start, and any one country that gets too far out of line will find currency appreciation itself addresses the problem. So, do we believe the US “dot plot” suggesting three rate rises in 2022, while the Euro zone does nothing? We struggle to.

Powell is still clinging to the lower workforce participation rate (which matters) as a signal to defer rate rises and not the unemployment rate (which is more closely related to vacancies) and hence of less fundamental relevance. While employment is great, it will still be unattractive if inflation (and fiscal drag) takes off, thereby holding the participation rate low.

This does still suggest dollar strength, while sterling like other smaller currencies always needs to be wary of getting too far out of line with US rates. But also, a need to fathom out the new look economy. To us, it does not seem service industries that rely on cheap labour are operating in the same world they grew up in. Certainly not if it is onshore.

There is a forced change in government consumption patterns (and hence employment), and this will also be telling. We are heading into quite a different market, when all this shakes down.

Sitting on high cash levels over Christmas, as we are, is pretty cowardly, but if you can’t see the way ahead, slow speeds are usually safer.

We do also rather agree with Chico Marx, this year at least.

Charles Gillams

Monogram Capital Management Ltd

Some Big Calls

First posted on 7th February 2021

US Markets: The ‘no-Trump’ response

We may learn a little about markets from the curious absence of Trump.

We had been confidently told that without him the US stock markets would fold, and as US markets collapse, these days so do global ones. Indeed, not just relying on the US, has become the fund management challenge of the last decade.

Well, he went, admittedly in a two-stage collapse, but he and the Republicans are out of office, yet the apparent upset in Georgia passed with barely a market ripple. Markets just went on up, unconcerned. Now some of that is their appetite for short term debt fueled spending, which even if you know makes little sense, it is folly to stand in the way of.

But beyond it, higher taxes and lower growth must be the consequence, if you are buying stocks on a 6 times multiple of earning the next two years matter a lot, but when buying them on the current S&P 500 forecast of 25.35 times earnings, that implies those later high tax years must surely be in the equation too.

Has the market priced in the downside?

So, what seems to have happened, is the downside of future years has been calmly offset against the short-term gains of a stimulus package: is that logical? It seems unlikely, if nothing else a big corporate tax rise is due, to notionally pay for it all, plus a fair slice of traditional “stick it to the rich” revenge legislation.

The assumption seems to be that the winners in the higher consumption aisle will be neatly offset by those who suffer from the new regulations. We are less sure and do feel the ultimate impact will inevitably be lower US growth.

Of course, tech might solve all, but then it is very richly valued already. It might solve the growth problem, but could still be loss making for investors, at these levels.

That is not to say that Biden put on a poor show in his advocating a “go big” package, he did it lucidly and with passion, a good speech.

For all that, when a new leader arrives and confidently asserts lots of economists (but notably not including The Economist this week) think he’s doing the right thing, it means trouble ahead. While his near certainty that the US would consequently be back to full employment by Christmas was touching, but absurd. The excess stimulus might get growth back to pre-pandemic levels, but that’s really not the same as employment.

The China issue remains big.

Another really big asset allocation call:

We are hearing ever more gruesome tales about East Turkmenistan, following on from decades of horrors from Tibet, both sovereign states seized by China in the political chaos after WWII.

If you see them like the other nations seized by Mao’s fellow imperialist Stalin, at much the same time, you will understand the repression. Although as ever with China, with a big dose of racism, against the 7% of their population who are not ethnically Han Chinese, plus of Communism, which still stands against any form of religion, be it Buddhist (Tibet) or Islam.

Will Biden care more or less than Trump about human rights? Well obviously, he will care more, as something is more than nothing. But will he be more effective than Trump, indeed do the Chinese find an unpredictable enemy with a penchant for sudden tariffs, harder to deal with, than a believer in the international order and gentle fireside chats?

Well here cynicism prevails: these are nations caught between empires, like Poland was for centuries; any tension in the international order will always see a land grab by their bigger neighbours.

I also believe Biden will find the proposed attacks on American consumption through both higher taxes and the removal of cheap energy and labour, can perhaps withstand also keeping Trump’s price rising tariffs in place. As notably he has done just that, to date. Indeed, he seems to be out-Trumping Trump on Federal procurement and protectionism.

But I still don’t think cutting China out of global trade, however barbarous their actions have been, is a runner. I think the vile abuses of power can go on, just as the EU has already handed a free pass to China’s torture chambers to plough on, by agreeing a new trade deal with no human rights teeth. So, in time, realpolitik will triumph with Biden.

It was I suppose nice to see China (after a pause for thought) suggesting locking up elected politicians in Burma, after the Army grew tired of holding all the cards, but getting no thanks for it, was a poor move. But there was a long enough pause to just tell the junta they didn’t mean it and were really rather pleased. A little more discord, more repression of the ‘tribal’ areas along their shared border, more sanctions to exploit, a few less pesky journalists, all are very much in China’s interest.

So, I see a curious dichotomy, in the Han Chinese areas, Tesla car plants, Apple phone stores, Starbucks a plenty, for a sophisticated technologically advanced middle class, will all thrive. While the minority non-Han areas will be pillaged for resources and labour and if they are good, be re-settled and re-educated and polished up for tourists. A bit like California in the 19th Century. So perhaps Xi is right, only China can split China, but then history suggests, it will, one day.

But not any time soon; you can take a moral position on Chinese racism, or an economic one on Chinese dynamism, but I am fairly sure the market will easily favour the majority.

This of course does create another ESG contradiction, the US high flyers rely on selling to the Han Chinese but are keen to exploit minority Chinese labour forces and natural resources. We can look forward to a great deal of sophistication in somehow disconnecting the two.

Efficacy of the Astra Zeneca / Oxford vaccine

Finally, I should mention the battering the EU and even perhaps the Euro (at a nine month low) has taken from the principled resistance to fudging the data exhibited by German scientists. The scientists are right, the evidence base for efficacy in the over 55 age group is indeed absent. Excitable politicians, including the normally precise Macron, have said it means it is ineffective, which it does not, only that proof is lacking.

Now that is presumably in part to cover the arrogant and inflexible EU procurement process, so full of checks and balances it strangles itself.

Boris’s vaccination stance

While Boris (faced with the same data) decided to wing it, correctly seeing that to save the NHS and his own electoral chances in May, he would rather give a potentially useless but harmless jab to millions of elderly disease vectors, than talk about due process. For once his disdain for the experts paid off.

The opposition in the meantime pleaded for a longer deprivation of our liberty by a longer pointless lockdown. Thank you for that suggestion.

Call it luck, if you will, but Boris has spent a long time practicing that ex tempore talent.

Proof might have been lacking, but it looked a jolly good bet. It sure was.

Charles Gillams

Monogram Capital Management Ltd