POWELL / GOVE : DROPPING THE PILOTS?

Jerome Powell looked ill at ease twice at his Wednesday press conference, with neither occasion related to monetary policy. While in the UK, Gove’s sidelining is the end of any chance of reform from this UK government.

Oddly when asked about his ‘hand in the till’, for bailing out his own family position in US Municipal bonds, Powell barely flinched. So why then is he worried?

The Powell press conference - what riled him?

He should be upset that the unemployment rate among black Americans is twice the level it was pre-COVID, at over 6% still. Given his pledge to hold the money taps open till that is fully recovered, which has for a while been clearly impossible without traumatic inflation, harming those same citizens, that should concern him.

This has long been Powell’s talisman to ward off the hard left, who are bent on two great goals, firstly taking over the reins of power by ejecting him and secondly finishing off Wall Street, as they so nearly did under Obama. Kamala Harris has not been in that triumphant position, at least not yet, so do the left really want to accept another deputy?

I doubt it.

So, the two questions Powell was riled by, were one about the new deputy governor, who has in this case the power to drive the regulatory agenda, mandated under Dodd Franks. Now, if one of Senator Warren’s acolytes can be inserted there, Powell will find life immeasurably harder. But for markets worse still,(the second question) was if Powell himself is chopped (Trump looked into it) before the recovery is complete. A weakened Biden has few other goodies to offer, if his portmanteau bill to throw $3 trillion of cash to his voters fails, scrapping a top Trump nominee at the Fed, might be the political trade-off.

While for Powell, as this all starts to get rather dirty, I could see him for the first time, asking if he was really that bothered.

The US recovery - stimulus, markets, and minorities unemployment

The rest was all telegraphed passivity, still pumping enormous stimulus into the US economy, long after the recovery is running hot.

The US 10-year bond resumed its gentle lapping sound against the low-rate rocks, the storm of inflation roared on overhead, and the shadow of crossed fingers, fell on every vault.

The market has turned, in the US at least, from worrying about ‘when’, to guessing ‘how high’, with, given the global malaise, some confidence that “not very” is the answer.

Chop the Chair of the Fed, and that delicate illusion shatters. While whatever his politics, shipping Jerome off the transom, will hurt those same beleaguered minorities most. We should never underestimate the zeal of a convert, and he is that.

Sidelining Gove

We have not seen that kind of zeal on these shores for over a decade. True, various short-lived moneymen have breezed through ministries, failing to unpick their form and function, scattered management speak and chums’ contracts around equally liberally, and left.

But lifting the drains, sorting the plumbing, fixing the boiler type reform, no, Gove is oddly (because he was useless at it) the last of those to fall. But he had the great merit of scaring people and driving legislation, which with the stodgy morass of public sector spend, is part of the battle. But the idea that he can either help on “levelling up” (which is just a catch phrase, and always will be) or pacify the Celtic fringe, hungry for real power (and unaware it does not exist) is risible.

Meanwhile, the Cabinet Office is quietly stripped of ministers, to be put back in the box marked “too difficult” once more.

A parallel with Chinese policies

This is like selling the inhabitants of East Turkmenistan down the road for some of Chairman Xi’s foggy promises on future coal fired power stations. It would be sad if it weren’t true.

Although China is now helping us return to a land beloved by investors, where money is scarce and hence actually earns a return. While risk still clearly comes in many forms; including Marxist morality, that is, if such a thing exists.

Big corporate failures do at least achieve that heightened risk awareness.

Charles Gillams

Monogram Capital Management Ltd

:) You might already know that 'dropping the pilot' is a famous cartoon by Tenniel from 1890 when the Kaiser dropped Bismarck.

EVERY DOG

Boris seems slowly to be turning into the opposition to his own party, which I suppose is not new for him. Meanwhile China also seems to be hitting an identity crisis. Neither bodes well for investors.

We apparently have a real budget due soon, but this vain Prime Minister seems bent on upstaging his own team, so we had a pile of tax rises and changes to tax law bundled out in a haphazard fashion in response to the endless (and insatiable) demands of one ministry.

A likely collision course with natural Tories

That pretty well defines bad governance, and these ad hoc excursions into major spending plans are a hallmark of waste and short termism. So, to me the investor headline should be about planning ahead for the Tory government to either fail in front of an exhausted electorate, or less plausibly given the large majority, to implode. But have no doubt that No 10 and the mass of the Tory party are now set on a collision course.

The extraordinary extravagance of the blunt furlough scheme has always been the fiscal problem, and it is hard to believe, as many bosses are clamouring for new migration to solve multiple labour problems, largely in some measure of their own making, that the government has still parked up a fair chunk of two million workers, on pretty close to full pay.

I struggle to comprehend that number in a hot summer labour market, nor do I see why employers would cling onto staff until October at which point, presumably they take a decision? Are these ghost workers? Already happily in new jobs, but having done a deal with their bosses to split the loot, their fake pay for not being? Are these people HR have forgotten or are too scared to fire? Will they really try to pick up work they put down eighteen months back, in a largely different world and probably for a now quite alien organisation?

Who knows, but the whole thing cost £67 billion (so far) and that’s what Boris needs back. I challenge anyone to give a lucid explanation of how his latest proposal “fixes” social care for the elderly. Nor to explain how in parts of the country like this, with no state care home provision anyway, it can ever be called “fair”. So, to me, it is just bunce for the ever-gaping maw of the state, and the idea, with Boris in charge, that it will ever be temporary or even accounted for, is somewhat risible.

What would “fix” social care is transparent, autonomous, local provision, not bullied by a dozen state agencies, not run by money grubbing doctors, not harried by property developers and absurd land costs, nor daft HMRC grabs on stand-by staff pay, and it needs to be highly invested in simple technology, all IT integrated with the NHS; not this crippled, secretive, subscale mess.

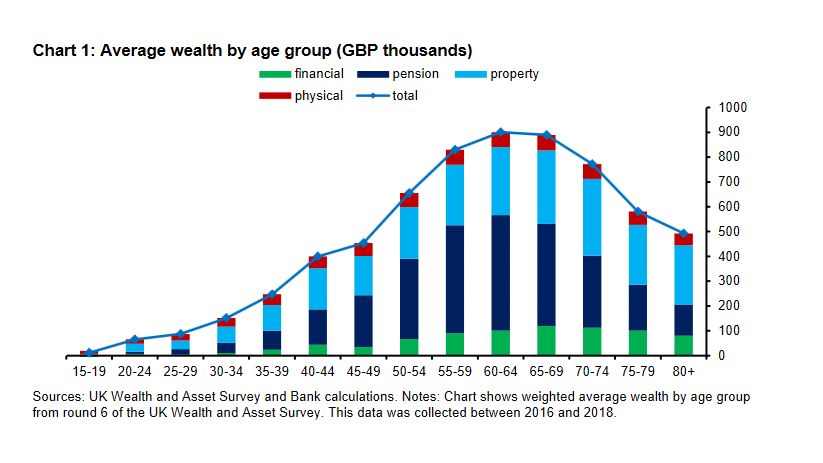

It is not that there is no problem, but it is as much operational as financial. A recent Bank of England paper looking at wealth distribution highlights how in retirement property comes to both dominate assets and also shrinks far more slowly with age.

(Sourced from this speech given at the London School of Economics, by Gertjan Vlieghe, member of the Bank of England’s Monetary Policy Committee.)

Of course, the crux here is seeing a family home as both an asset and an essential for life. That is the distortion, and this fiddling with care rules attacks the symptom, not the cause.

Can you trust a word he says?

So, now tax on income rises, a broken promise, employer tax rises, broken promise, the ‘triple lock’ on pensions is ditched, broken promise, and to top it off those working beyond normal retirement age (now 66) get a 25% tax penalty, via another broken promise. Oh, and if you are mug enough to save, then dividends will get hit too.

Again, there is a real problem but this is by no means a logical answer either: I guess the Treasury were applying heat on excess debt, and this is sand kicked back in their face, but it shows no sign of anyone solving anything. The UK has both high debt levels and no supportive currency block around it, sure France and Italy look bad, but they have Germany to help. The UK does not. Hence the anxiety.

So, Boris has had a fine Cameron-like bonfire of dozens of electoral promises; the worm turned on Cameron (and Clegg) when he couldn’t keep his word, and so it will turn on Boris. This time he won’t have Corbyn as the pantomime bete noir to bail him out. Indeed, Kier Starmer’s response linking this problem to inflated property prices is remarkably prescient, even if his typically confiscational solution is not.

These tax levels (as a % of GDP) have not been seen in fifty years, for an economy with a noticeably less effective grasp on government expenditure and a rather less globally competitive commercial base.

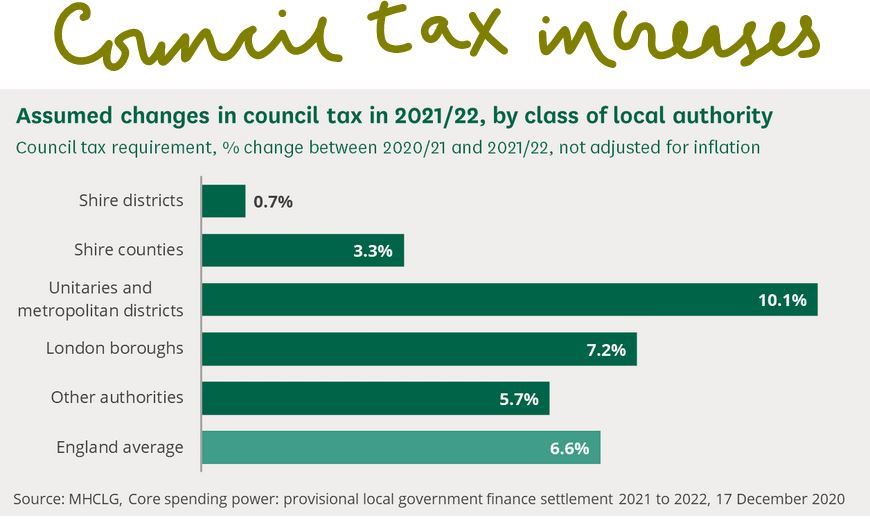

While tax rises are emerging everywhere (see below), and public service reform has become a simple money equation, need more service, spend more money, a dangerous one-way road.

Source: from this primary report

While notably, ‘buy to let’ is again left untouched. London house prices have doubled in this century, the FTSE 100 has moved from circa 6800 at its late 1999 peak to 7030 now and remains below pre-pandemic levels. So clearly this is not the time to hit the investors in jobs and business, who have had a 5% nominal gain (that is a 60% real loss) in twenty years and yet to leave the buy to let rentiers trading in second-hand hopes, with their 60% real gain in that time, untouched.

And don’t give us the dividends argument; the buy to let plutocrats get plenty of rent and all their sticky little service charges. This measure simply hits the workers and investors in business and pampers the bureaucrats and the rentiers. It makes very little sense, unless you are a senior civil servant or a retired prime minister, like Blair, of course.

Chinese insularity - the new version

Meanwhile China I feel is now detaching itself from both the rule of international law (in so far as it ever bothered) and more interestingly the world financial system. It may indeed end up better off, but for now (and this is also a change from much of the last 50 years) it does not feel it needs to attract external capital.

So much of its trade and capital markets engagement has been predicated on securing capital; this is an odd and novel twist. Although perhaps a logical response to the West, who rather than conserving capital as a scare resource, are immersing the world in torrents of surplus cash and inflation.

Much of China’s policy about their own global investment (so outside China) also used to have the same theme, driven by the desire for returns, influence and to hold their own export-based currency down.

But no more, it seems, and their inherent desire for autarchy, the hermit kingdom trope, has only been emphasized by Trump, WHO and the madness of the internet. It apparently wants to be the new Germany, (no longer the new USA), so it will be insular and conservative: cautious, not driven mad by debt and the baubles it procures.

Well, if true it will be different, whether it can really be done, without a wave of disruptive defaults is unclear, but don’t doubt the length of vision, so unlike our own government. While a theme of this century has also been where China leads, the rest must reluctantly follow.

Even a dog has its day, but for investors both the UK and China now feel significantly more canine than at the start of the summer.

ESG : Being All Things to All Men

I have been attempting to not write about ESG all year, as passions run high, and it feels to be more about faith and politics than Environmental Social and Governance (whatever that is) itself, as they encompass an incredibly wide set of issues, now being squeezed remorselessly into a few tick boxes.

However, I have been greatly enjoying Simon Schama’s magisterial tome on the Batavian Republic, as the Netherlands were known during what we loosely call the French Revolutionary wars. The analogies to the situation today are startling.

Can you Take a Position on ESG Issues?

In the environmental universe, I personally tend to be far more a “dark green”, than a “light green”, which in very crude terms holds that sustainability is not a matter of work-rounds with the “same as before” levels of consumption, but of a reshaping to avoid the extraordinary growth in raw consumption seen over my lifetime. More Monbiot than Musk, you might say.

Yet on trade, by contrast, I would ally strongly with the ‘Social’ part of it: nothing frees a nation like free trade, and nothing builds prosperity so fast. Just ask the Chinese.

A new Form of Colonialism?

Free trade also includes the free movement of capital, so that the relentless red lining of the most impoverished third of the planet on the grounds of failing to meet our Western standards of governance, feels very much like old colonial exploitation.

Effectively you’re saying – ‘yes, do sell what you like, made by who you like, using what you like, but just not to our markets’.

How can anyone be in one place on all of these often-opposing issues? If you are, the investable universe shrinks to nothing, or indeed paradoxically becomes everything. I have seen ESG bonds where China and Qatar were the top holdings, I am sure on perfect ‘E’ box ticking, but not my idea of either the ‘S’ or the ‘G’ part of it.

Governance, the most Elastic Concept of all?

While in my experience, few things have so powerfully increased inequality as remuneration committees, festooned in ways to line the pockets of directors, and singularly toothless in their stated aim. But all it seems fine on the weird ‘G’ criteria.

There are many other fraternal and earnest slogans now hiding deceit. Several of the current entrepreneurs most carefully cloaked in greenery and its social equivalent, have a decidedly old-fashioned view of governance, a fondness for non-voting shares and other tricks, and boards stuffed with their mates, which then also leaves the substance of the ‘G’ part well short of the mark.

So, to me ESG ends up as so wide, that an investor who really cares must pick and choose where to place the emphasis. Yet even this is seldom possible, in part because so many collective instruments are already being packaged in strict tick box compliance, which massively restricts your options.

The curse of all index investing is you end up taking a set of equities typically based on their market capitalization, so “desirable” stocks by definition end up in wider and wider sets of indices. As so much is now index investing, you are then forced to acquire both sheep and goats, with little chance of avoiding one and adding to the other.

However, as a fund manager you must always play a twin game, of either allocating capital to where it is most productive or allocating capital to where it is most popular. Clients tell you they desire the former, so they want good ESG credentials, but actually want to have the best return too, in other words the latter.

Governments, as China is now clearly showing far prefer (as they must) the productive to the popular. Popularity is proving dangerous in that market, as therefore is for now, index investing. Just as you pile into owning the latest media sensation, the state starts destroying it, almost a re-run of our experience in investing in UK banking.

All of which leads me to conclude that like anything else in markets, ESG can be good value, but can also be poor value; what it can’t be is always wholesome. Investors should realize that if it is not to be all things to all men, it must also ultimately cause them losses as well as gains.

I could add a line on Jackson Hole and Jerome Powell, but that is all that it deserves, nothing new was said.

I notice that he too has become, skillfully, all things to all men.

Charles Gillams

Monogram Capital Management Ltd

Holiday reading – Simon Schama – Patriots and Liberators.

Simon Schama unpicks the eternal power and politics questions, seen through the simpler although less familiar lens of the Dutch.

I now finally understand what Camperdown was all about, so apparently it is not a racecourse, after all.

Although the Anglo Russian invasion of Holland remains mysterious, it does remind us how fleeting our alliances are.

The British showed considerable skill in repeatedly landing in Holland, looting the place, seizing much of the Dutch fleet, and then executing a negotiated evacuation, when they had clearly failed in their main mission of “liberation”, without too much embarrassment: an under rated skill it seems.

The sheer impossibility of nation building by force and myriad other democratic puzzles were exhaustively thrashed out by the Batavians, under the baffled eyes of the French invaders. Nothing changes, it seems.

While the sections on taxation and local government are rather strangely relegated to near the end, but feel to me, something of a connoisseur of both, perpetually modern. This was the period when the old inherited ways were first discarded, and our new ‘modern’ systems sketched in.

Their arguments over decades are now ours too. The clash of a European superpower and democratic freedom rings true still, the crippling burden of an overmighty, half blind and deeply corrupted centre remorselessly subverting the myth of its own creation by greed, the utter folly of war and the deep atavistic permanence of old boundaries are all visible.

Inflation: The elephant in the room?

Inflation and how persistent it is, now fascinates us although we will skip how that relates to US bond yields, as that currently makes no sense. We’re also pondering the recent high performance from non-US markets.

We signaled inflation as a forthcoming problem well over a year ago, and slightly oddly not for either of the two reasons now cited so often. The received wisdom, that it is all about freight rates and used car prices, identifies specific issues we had not spotted.

Freight and used cars – really?

The freight issue seems to be a jumble of factors, dominated by having the ‘wrong’ demand structure, so in any movement of goods (or people), one way traffic is also the worst, if you can get the return route paid for by someone else, you will always halve the cost. Hence the obsession on most mass transport with return tickets. Sudden demand shifts destroy that balanced economy. But clearly there is more to it, so poor port capacity, extra flows created (or existing flows destroyed) by COVID all matter, all that PPE displaced other goods, while grounding airlines eliminated vast amounts of high value hold space.

But all of that, the natural creation of new capacity (that is making more containers), or simply activating more shipping from lay ups, will create new supply, and we therefore recognize that whole process as a fairly short-term spike.

As for used cars, well, I can see from the congested roads that no one is using public transport, but with global over capacity, how long will that surge in demand for cars last? In general shutting car plants due to excess capacity still remains the trend. While flaws in the too tight “just in time” schedules have been apparent for a while, not helped by almost bespoke production, but that too is all probably transient.

After all, a hire car can be any colour, as long as it is black.

So, what did worry us about inflation? Capacity and competition remain the two drivers.

It was capacity, as either the number of viable business units has to decrease, if the costs per unit increase, or the price per unit sale must rise, hence inflation. This is obvious to most, although it seems not to many Central Banks. For a while any business will, it is true, keep going, even if only generating a marginal contribution, but soon it must either cease trading or lift prices. Companies just don’t sit about making losses, in the real economy.

The other part is competition, as the number of operators in a market decrease, the survivors gain greater pricing power to raise prices, while no one builds any new capacity simply to suffer losses. You can easily see these two dynamics play out in the coffee shop sector (or indeed with wine bars and public houses). COVID eliminates 50% of the capacity, by enforced social distancing. Takings must then also fall by 50%. You can prop that business up by furlough, or tax cuts, or eviction bans, but sooner or later the owner will conclude that in a fixed physical space, a 50% revenue cut just can’t work.

With operators in both those sectors and indeed many others deciding they have had enough and don’t want to face mounting debts, the capacity is then lost and the incentive to replace it is weak, so competition inevitably drops.

Looking back at the hire car sector for a moment

We are told it is price inflation caused by a temporary shortage of cars, but that sector famously is full of border line survivors, the margins are wafer thin and often come down to the residual fleet value. Several big firms have also dropped out through insolvency; of the rest many only ever survived on the twin props of residual fleet value and extended manufacturer credit.

Do you think high secondhand values are making them expand their fleets? Not that plausible. More likely they are cashing in. Nor do auto makers need to restock them on vastly extended credit terms, just to keep their own production lines running. New car sales to the sector are always at low margin to bulk buyers. So that’s not likely either.

We think it is quite possibly inflation from capacity cuts and weak competition, and that is nothing like as transitory. That is far more durable, not a brief supply side spike. Turnover is vanity, profit is sanity, as industrialists say.

In short Powell et al want to see no inflation, want to tell their political masters it is all fine, that they can keep running the engine hot, but having skimped on the engine oil, it seems rather more likely that running hot will simply seize the engine. At which point they must either coast to the hard shoulder or apply the handbrake of interest rate rises, before the economy blows a gasket.

Currency and the momentum model.

The other note of interest to us is that non-US markets are starting to flash up on momentum boards as exceeding US returns over some time periods, in particular in GBP comparatives.

In dollar terms the momentum is in the S&P 500 and NASDAQ. However, in sterling terms it is moving. We have noticed Europe shifting ahead for a while, but we were surprised to see our GBP momentum model now drawing our attention to Latin America.

Now a lot of these models (ours included) are very sensitive to the recent past (that is the momentum we care about, after all) and that means there are big moves to fall in or out of the sequence, so care is needed. But despite the headline turbulence and distress in the Latin American continent, it has forces in its favour; the index is dominated by big mining operations, closely followed by oil companies, then banks, which are seeing rates rise sooner than in the rest of the world, and then (often Mexican) consumer goods.

They will find the weaker US dollar helpful in some sectors too, but will especially enjoy the vast demand surge (and short supply line to) the US. So, all in an index with some good reasons for outperformance, despite the political noise.

Is Sajid now a factor to note? Rapid reopening will probably also continue.

Talking of politics, I don’t see the renewed ban on French holidays (or rather the absurd elongated quarantine on return, regardless of vaccine status), as anything to do with COVID. Rather it is a shock coming from the always unstable Tory politics, where the return of Sajid has created the first node of a genuine “not Boris” grouping, as a minister now too valuable to be left out in the cold.

Boris can’t bully him twice, without a major loss of face, so some of the other pretenders to the leadership want to take him down, by sabotage to his policy of an overdue full and proper re-opening.

Shapps, who dreamt up the absurd new ban, it seems wants to usurp the health portfolio, and apparently feels put out at being left in a dull and dangerous ministry, hence his attempt to claim territory and undermine a cabinet foe. However, I think his manoeuvre makes little difference to the overall thrust of government policy on rapid reopening.

We also note, that at long last the destructive and stupid attack on UK banks, by enforcing a dividend ban, when they were awash with cash, simply out of political spite, has been ditched. I suspect it is too late to reverse long term damage to the sector, but even if a year late, common sense is welcome, as is evidence that the colossal 2020 state seizure of power, is at last being pushed back, at a few points.

Last April/May I was writing about these kinds of issues, now sitting in this book, if the more regular amongst my readers would like to take a look – one of the measures has to be consistency of approach, after all. The second volume is under preparation.

Finally, we too will take a summer break, returning to this just before the August Bank Holiday, as summer draws to a close.

We wish you an enjoyable break and a well-earned rest from what has been a crazy year.

Charles Gillams

Monogram Capital Management Ltd

18.07.21

ALL QUIET: Covid and UK Property

A brief glance at an excellent first half for investors: thoroughly “risk on” for the first quarter, but a slower but still an upward grind thereafter. Not that such arbitrary dates matter. What does count is what can make it kick on from here?

Covid patterns

So, first a glance at COVID, or rather our reaction to it. The disease itself is now less important in most OECD economies, they have the capacity to deal with it, vile though it is, and the vaccine numbers are rising steadily, faster than we expected in the UK.

This is a screenshot from this website at Johns Hopkins University : https://coronavirus.jhu.edu/map.html

In raw demographic terms, in most places it is barely a flicker on the remorseless upward march of global population growth, but the extraordinary evasive action being taken mattered much more, and I see little sign of that abating.

Watch a dynamic map of all births and deaths at this site: https://srv1.worldometers.info/world-population/ (these figures include all deaths, not just from Covid 19.)

One of the key issues is that, for whatever reason, it is prone to sudden spikes, the only defence to which is almost complete (90%?) vaccine coverage. Indeed, the spikes can clearly ride quite widespread vaccination, higher than originally thought. But the spikes last weeks, perhaps a month, and for most of the year, most places are not experiencing them.

The trouble, especially in the UK, is our muddled policy response is to take down the economy on a semi-permanent basis, almost as a fetish against the lurking evil. To put in place colossal support measures for spikes that are transient is both cripplingly expensive and turns emergency response into embedded base cost. We are on a constant war footing, even when the enemy has seeped away to regroup.

So, despite Mr. Javid’s optimism, we do expect the bureaucracy to cling onto extensive controls, that limit capacity in public services and many consumer sectors. I had hoped that the ridiculous restrictions would bear down on the elite’s summer holidays, but I now understand they don’t care, as they clearly don’t obey them anyway.

HOW MUCH MORE DELAY CAN THIS 'REOPENING TRADE' TAKE?

Which brings us to two thoughts, firstly the re-opening trade is shrugging off some mighty setbacks, and very little of the run up from last November was based on controls extending into 2022.

At some point balance sheets will start to crack, and values will then retreat.

Commercial property sector

The other is a more sector specific concern, but also a straw in the wind, in the extension of the UK commercial eviction ban well into 2022. I don’t follow the logic of that, it is a significant ongoing seizure of private property rights, it is not clear to what end. It is not protecting jobs, unless furlough is also to be extended. It appears to assume businesses can occupy premises rent free for an extended time period, although the Government also suggests (slightly oddly) that much of their business support package (mainly loans, with government backing) can be used to pay rent.

Not that I care much for commercial landlords, who have long been over protected in the UK and exploitative, but it is to me, an odd move. We looked at real estate earlier in the year and expressed support for the TR Property Investment Trust in particular, in February, after which it has been on a run. But reading a quartet of March year end REIT annual accounts, I feel rather less sanguine: those are British Land, Land Securities, Helical and NewRiver.

The trouble here is they got hammered last year, with their March rent collections a mess, and double figure valuation drops on the retail side, they have been hammered again this year, with similar double figure write downs, and now it looks like they could be hammered for the current year too. That’s a lot of damage for the sector.

Office rents are holding up, collections are better, surrenders fewer, but they are running hard to stand still, with typical average lease lengths in single figures; this brings a lot of renewals too close for comfort. Time off debt maturities is also becoming significant.

Some Specifics on British Land, Land Securities, New River.

Equally clearly a lot of London occupiers, in particular, will have spare space, probably well into 2024 and maybe forever. Successive asset write downs, keep eating into the debt cushion, rates are low, so debt service is not an issue, but covenants are tightening, cash flow for development is getting squeezed and banks are not sitting back, just because the tenants have a state license not to pay.

They do differ of course, British Land is fairly serene, based on London offices. Land Securities having been boring for so long has appointed a new team, from the student accommodation and logistics worlds. Granted both were good performers in the last decade, but they are talking of ditching much of the existing portfolio, to chase development schemes. Brave if nothing else, one might say. Helical is smaller but goes for ultra-high quality office refurbishments and expansions, with tenants who can pay for quality, but each of their complex inner-city projects can take years to get through planning and their growth depends on a steady stream of them. After current ones complete, there will be a hiatus.

While NewRiver, always an aggressive high (and at times uncovered) yield stock, also looks strange. Debt is substantial, and another double figure fall in values could be harsh. Granted that would take more of its yields into double figure territory, in areas where demand (and alternative uses) should really provide a floor. But it also flirted with a badly timed foray into pubs, and their valuers are (to no great surprise) saying valuations for those are in the “who knows?” realm. Meanwhile the finance man is apparently jumping ship to lead a spin-off of the licensed premises, which sends some quite odd signals, although maybe holders have tired of his complex skills.

This leaves a more bifurcated market than ever, but with the risk of overvaluations both in the good stuff (last mile logistics in particular) and storage in general, and in residential.

By contrast UK retail is looking ever more wounded. It has been a great reopening trade, but unless the runway is really getting cleared, take off may now be too late for some.

Meanwhile Boris can’t seem to let go, having gained control, freedom is clearly an unattractive option to those in power. If that stays the same, we can see a perfect real estate storm brewing, if and when liquidity dries up a little.

The umbrella organisation, RICS, has in the mean time this summary to offer as its full market survey results.

Politics in the constituency of a murdered labour politician

Finally, the odd thing about Batley and Spen, was the idea that the Tories could win. I looked up the odds on Labour last week, at 4: 1 against, I found them most attractive. And that was based on my wrongly writing off Gorgeous George, who mercifully is one of a kind.

Without his strange allure it was and is very solidly Labour. Another non-story, I fear.

Charles Gillams

Monogram Capital Management Ltd